“When everybody is digging for gold, it’s good to be in the pick and shovel business.” – Mark Twain

Biotech is booming. Between technological developments in artificial intelligence and the GLP-1 weight loss craze, people are flocking to the medical space to capitalize on this once-in-a-lifetime opportunity.

Today, there are over 12,387 biotech companies worldwide and over 3,740 in the United States while the global biotech market is projected to reach $5.68 Trillion by 2033. This represents unprecedented demand over the coming years and hints at a major opportunity for those willing to take the leap.

But the biotech space is grueling. On average, the cost to make a new drug is over $1.4 billion, and more than 90 percent of drugs fail to reach commercialization. Not to mention the formidable feat of competing in a market saturated by industry giants and early-stage hopefuls.

However, there are ways to capitalize on this booming industry without subjecting your portfolio to the typical risks tied to biotech stocks.

In this article, you will discover a telehealth company firing on all cylinders through its direct-to-patient platform. This platform connects patients with doctors and drug manufacturers, creating a network effect that compounds organically, without the typical strains of a biotech business.

To date, the company serves over 235,000 recurring customers, produces a positive free cash flow, and maintains an average gross margin of 87%. It also has generated an annual return of 128% for shareholders since 2018, is up 202% over the past year, and trades at a market cap of just $313 million.

This leads me to wonder whether it can deliver uncommon returns in the future or if the company has reached its peak. Either way, the prospects are too attractive to ignore.

Understanding LifeMD

LifeMD (LFMD) stands out among telehealth businesses today. Unlike many competitors, it has established itself as a leading platform in the growing virtual primary care industry.

To achieve this, LifeMD made significant investments in its technology infrastructure, creating a seamless experience for patients, physicians, and business partners. This project involved over fifty software engineers working closely with the company’s medical, operations, and marketing professionals to “design a platform capable of facilitating complex virtual and in-home healthcare at scale” (Justin Schreiber, Chairman & CEO, 2024 Shareholder Letter).

LifeMD’s platform now features:

- A robust electronic medical record (ERM) systems

- Case-load balancing and scheduling nationwide

- Customer relationship management functionality

- Remote and in-home lab testing

- Digital prescription capabilities

- Patient-provider audio/video interfacing

- Mail-order and brick-and-mortar pharmacy services

- In-home healthcare tools and more!

These features make LifeMD one of the most comprehensive solutions in the market, offering patients unmatched access to physicians and pharmacies at a fraction of the cost.

U.S. healthcare system | LifeMD

So how does LifeMD make money?

The majority of its revenue comes from subscriptions to its platform. With over 235,000 active subscribers, these accounted for 97% of its revenue in Q1 2024.

Behind the scenes, LifeMD has a three-pronged business model designed to serve its patients and enhance the customer experience:

Direct-to-Consumer Virtual Primary Care (D2C): D2C is LifeMD’s flagship offering, providing 24/7 access to affiliated providers for primary, urgent, and chronic care needs. This mobile-first, full-service solution offers virtual consultations and treatments, prescription medications, diagnostics and imaging, and wellness coaching; customers also benefit from discounts on lab work and prescriptions at over 60,000 pharmacies.

Additionally, LifeMd rolled out its GLP-1 Weight Management program through this segment in 2023. With the GLP-1 market projected to be worth $100 billion by 2030, LifeMD has direct access to one of the fastest-growing markets in the world. Already, the company has expanded its patient count from 22,000, in 2023, to over 50,000 today.

Direct-to-Patient Telehealth Brands (D2P): LifeMD owns several medical brands addressing unmet healthcare needs:

- RexMD: A men’s telehealth brand offering treatments and prescriptions for various conditions, serving over 500,000 customers with a 4.6-star Trustpilot rating.

- ShapiroMD: A solution for men’s and women’s hair loss, treating over 265,000 patients with a 4.9-star Trustpilot rating.

- NavaMD: A female-focused dermatology brand providing dermatologist assessments and prescriptions for various conditions.

- Cleared: Offers personalized treatments for allergies, asthma, and immunology, including in-home tests, prescriptions, and FDA-approved immunotherapies at 50% cheaper than brand-name competitors.

B2B Telehealth Partnerships: In 2023, LifeMD began partnering with other businesses to enhance its network:

- ASCEND Therapeutics: A specialty pharmaceutical company focusing on women’s health. LifeMD helps improve access to ASCEND’s EstroGel treatment while ASCEND features LifeMD’s services on its website and pays service fees.

- Medifast: A health and weight loss company leveraging LifeMD’s platform to provide a clinically supported weight loss program, including GLP-1 medications. Medifast invested $10 million in collaboration support and an additional $10 million for an ownership stake in LifeMD.

Additionally, LifeMD holds a 73.32% stake in WorkSimpli, a SaaS provider for workplace and document services. WorkSimpli offers:

- PDFSimpli: A platform for PDFs

- ResumeBuild: A platform for resumes and cover letters

- SignSimpli: A platform for digital signatures

- LegalSimpli: A provider of legal forms for consumers and small businesses

WorkSimpli boasts over 166,000 active subscriptions and generated $13.3 million in revenue in Q1 2024, accounting for 30.1% of LifeMD’s revenue for the quarter.

Overall, LifeMD provides a comprehensive, diversified, and scalable solution. The company invests in fast-growing markets like the GLP-1 weight loss market while maintaining steady growth in other areas of its business.

In the next section, we’ll discuss how LifeMD is building a durable competitive advantage and what it will take to sustain it.

Why is LifeMD Different?

Network effects are crucial for the long-term success of any platform that connects businesses and consumers. The basic idea is that as more customers join, more producers and suppliers are likely to follow, and vice versa. This organic growth reduces the need for heavy investment because the increasing user base attracts more participants naturally.

For LifeMD, the aim is to attract as many repeat patients as possible, which in turn draws more providers looking to serve them. The key to achieving this is a patient-centric approach that prioritizes high-quality care.

LifeMD delivers on this through the convenience, optionality, and affordability of its platform.

For one, the company’s 50-state medical group and 60,000 affiliated pharmacies ensure that patients can access medical professionals and prescription medications no matter where they are located.

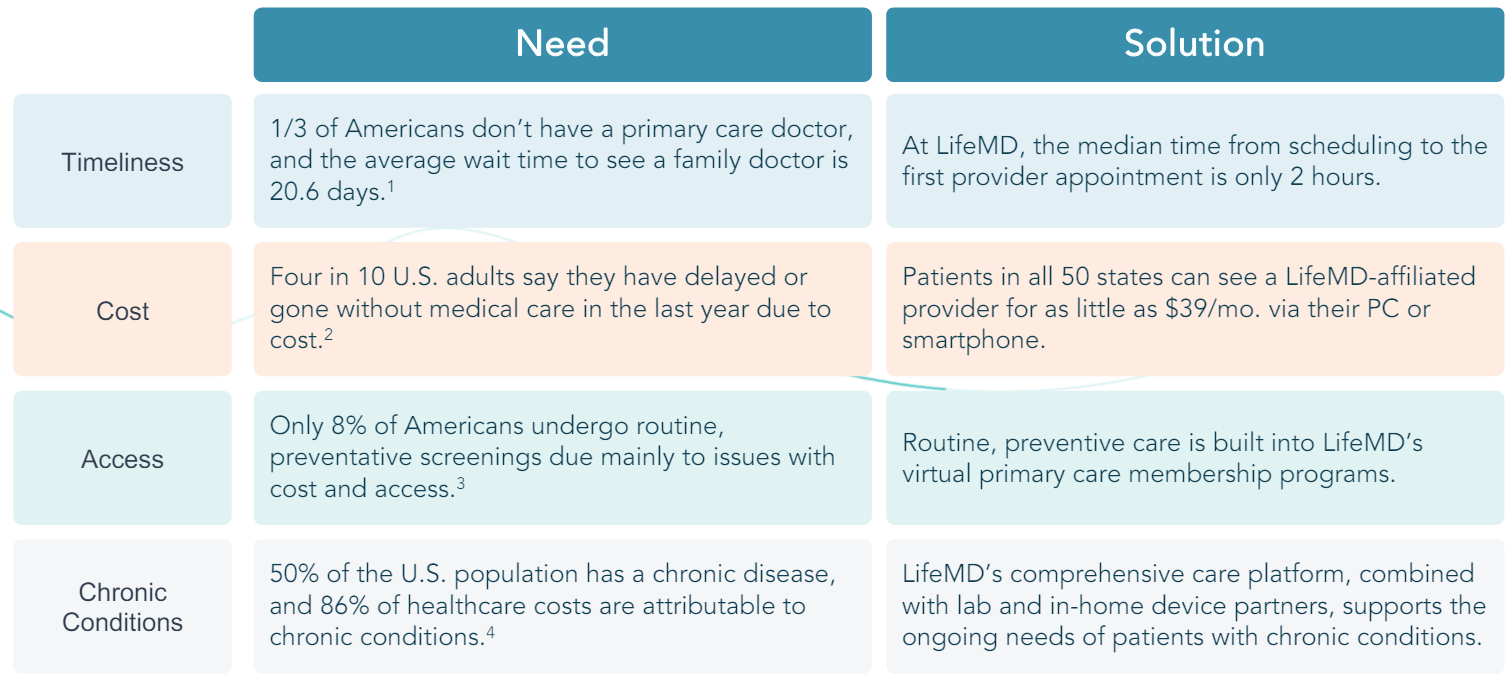

Second, LifeMD’s 24/7 customer support channel, comprehensive services from assessment to delivery/pick-up, and the speed of appointments mean that patient needs are met promptly. For example, the median time from scheduling to an appointment on LifeMD is 2 hours, compared to 20.6 days for a family doctor visit.

Third, the full-scale electronic medical record (EMR) system allows patients and practitioners to track clinical data effortlessly. Finally, the broad range of medical conditions LifeMD addresses (over 200) enables it to serve a larger customer base than most telehealth platforms.

While these features are essential for attracting patients, what truly sets the platform apart is the quality of care. LifeMD boasts an average physician rating of 4.9/5, reflecting the high level of patient satisfaction and the quality of medical professionals it provides. Maintaining this performance will be crucial as the company scales.

So how does LifeMD stack up against competitors?

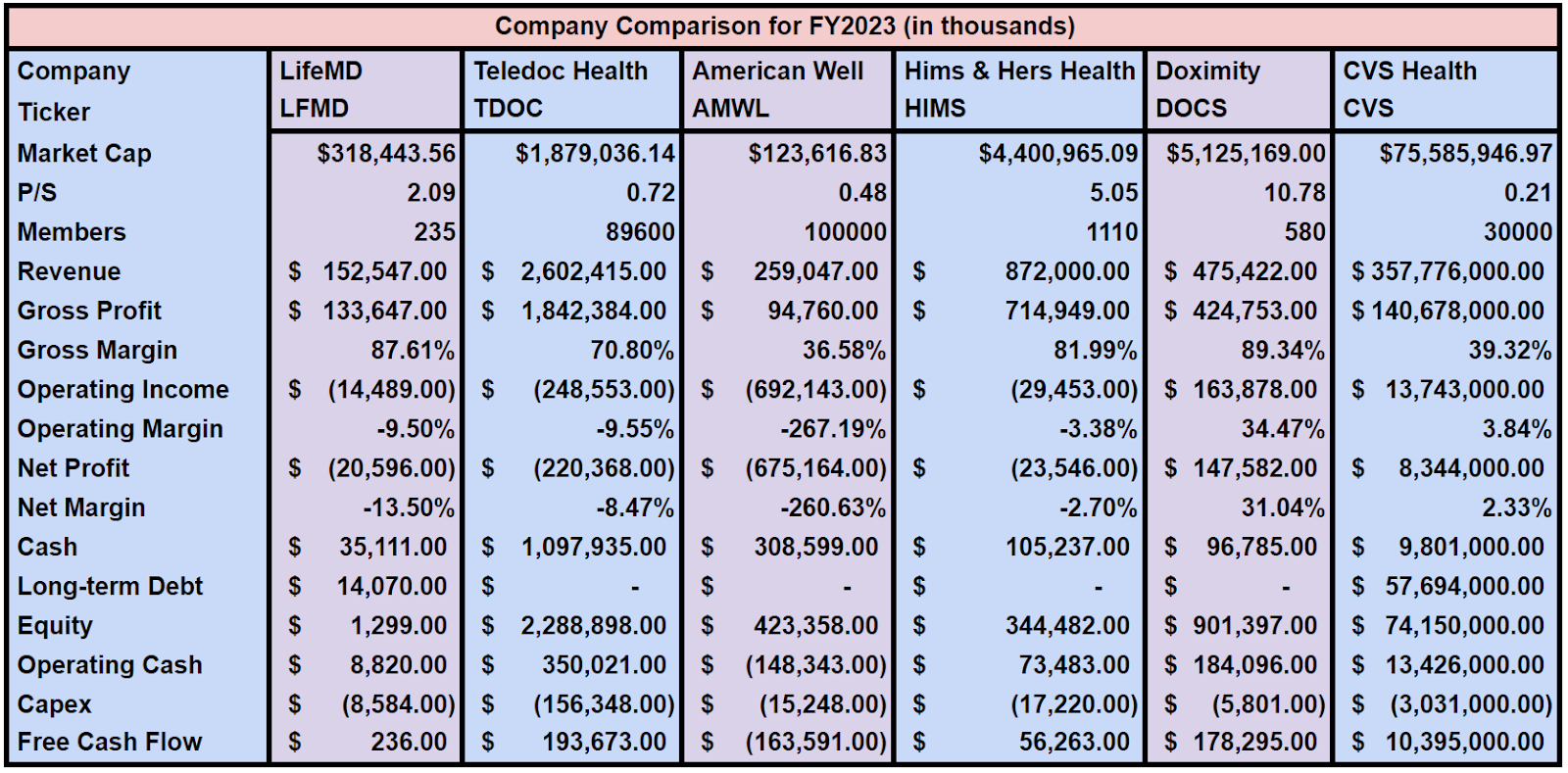

LifeMD competes in various markets, including virtual primary care, weight loss, men’s and women’s health, dermatology, and traditional healthcare markets like drug store chains and independent pharmacies. Key competitors include Teladoc (TDOC), AmWell (AMWL), Hims & Hers Health (HIMS), Doximity (DOCS), and CVS Health (CVS).

Overall, these competitors have larger user bases, with subscriber/user counts of +90 million, +100 million, 1.11 million, +580 thousand (providers), and 30 million, respectively. Each targets markets that overlap with and are unique from LifeMD. From this perspective, LifeMD has the weakest network effect to date, although it is significantly smaller than most of its competitors.

However, size isn’t everything. Among businesses targeting patients (excluding Doximity, which is physician-first) and with similar market values (excluding CVS), LifeMD has the strongest gross margin at 87.61%. This, along with an improving financial condition, demonstrates the feasibility of its business model and competitive position. It remains to be seen if LifeMD can maintain its margins as it scales, but for now, it presents a compelling case for being a strong player in the market.

Ultimately, to become the go-to telehealth platform in the United States, LifeMD will need to capture more market share by attracting more patients and providers.

Assessing LifeMD’s Leadership

One of the things that stands out about LifeMD is the management team it has assembled. Chairman and CEO Justin Schreiber presents himself as a sophisticated executive who is determined to create long-term shareholder value.

As mentioned previously, since taking over in 2018, Schreiber has delivered compound annual returns of 128%, compared to just 13.35% for the S&P 500. This success is the product of a sound execution strategy—developing, commercializing, and scaling its telehealth platform—and intelligent capital management throughout his tenure. It also reflects a willingness to capitalize on high-growth markets like GLP-1s, where patient accessibility has been quite limited.

Another important aspect of Schreiber and his management team is the high level of insider ownership within the business. Between the executive team and the board of directors, management owns roughly 25% of LifeMD.

This is unprecedented for publicly traded companies and speaks to the conviction its leaders have in the business. It also ensures that management acts in the shareholders’ best interest, given that their wealth is directly tied to the business over the long run.

As Schreiber puts it, “We take the management of your investment very seriously, treating your money with the same care as our own, and are dedicated to maximizing the value of your investment.”

LifeMD’s Financials

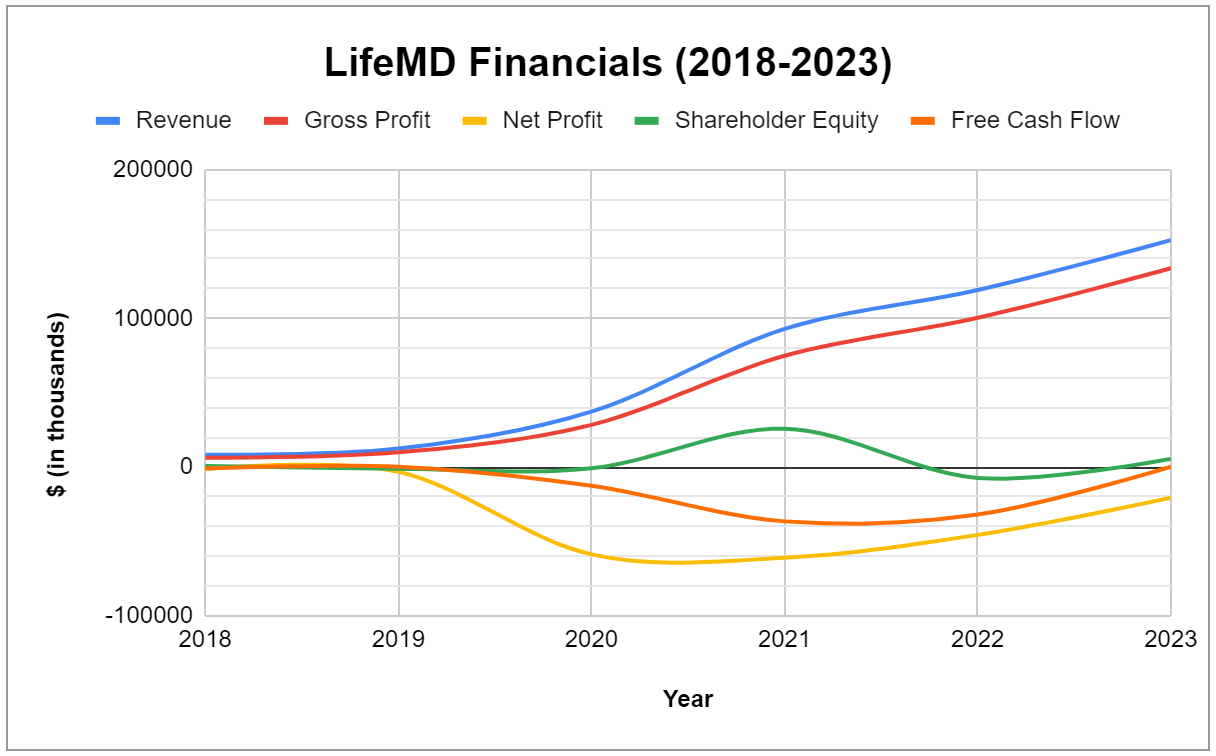

LifeMD’s financial trajectory is heading in the right direction, though we would prefer more consistent profitability.

Despite this, the company is experiencing remarkable growth. From 2018 to 2023, LifeMD compounded its revenue, gross profit, and shareholder equity at annual rates of 78.90%, 84.05%, and 46.67%, respectively. Additionally, with a strong cash position of $35.11 million and long-term debt of $14.07 million, LifeMD is in solid financial health overall.

In this next phase, maintaining profitability while scaling is critical for LifeMD. Cash is the lifeblood of any business, and a company that can generate it organically faces virtually no risk of failure.

From what we’ve observed, LifeMD seems well-positioned to continue its growth strategy without negatively impacting shareholders in the long run. However, the telehealth market is highly competitive, and LifeMD must deliver exceptional value to increase its market share.

As long as LifeMD operates diligently, penetrates new markets, and positions itself well for the future, it appears poised to provide above-average returns in the coming years.

Points of Criticism

Though LifeMD is shaping up to be a quality investment prospect, there are points of contention that you should be aware of.

#1: Why is LifeMD’s subscriber count so small?

The company’s platform has been operational since 2020, yet it only has 235,000 active subscribers. To be fair, the company has grown its active subscribers by 31% year-over-year, but this is still far behind other telehealth platforms mentioned earlier.

In its investor presentation, LifeMD lists a series of needs it addresses through its digital platform:

- One-third of Americans don’t have a primary care doctor.

- The average wait time to see a family doctor is 20.6 days.

- Only 8% of Americans undergo routine preventative screenings due to cost and access.

- Forty percent of US adults delay medical care because of costs.

If LifeMD plans to be the go-to platform, it must find ways to increase its subscriber count more quickly. There are too many players in this market to grow slowly, and the cost of losing customers is too high.

Once a patient signs up, the likelihood of them switching to another platform diminishes substantially, as long as their needs are met. While it’s clear that LifeMD provides a high-quality solution, it will be all for naught if they fail to attract customers before the competition.

#2: Does LifeMD’s WorkSimpli investment make sense?

WorkSimpli is a quality business, delivering EBITDA of $16 million and revenue of $54.39 million in 2023. These are solid numbers for a secondary business and help LifeMD diversify from its primary offering. However, the position seems odd given that it operates in an entirely different market.

That’s not to say WorkSimpli is a bad investment, but if LifeMD believes its telehealth platform is its golden goose, why not liquidate that position and use the capital to enhance its primary offering?

In all, LifeMD’s weaknesses are limited as long as it continues to grow and improve its competitive position. For now, these points of contention pose minimal risk to the company.

Final Thoughts

It is hard to ignore when a company produces a 1-year return of 251.87% and a 5-year CAGR of 128%. This is phenomenal growth by any measure and LifeMD deserves its flowers for its performance over the past five years.

Though the company does seem smaller compared to other telehealth platforms and its financial performance is solid at best, management’s ability to invest capital effectively and the quality of care it provides gives us confidence that LifeMD has the means to develop into a top-tier business.

The question is whether it can sustain this run and if it has what it takes to deliver market-beating returns moving forward.

Disclaimer/Disclosure:

We are not brokers, investment, or financial advisers, and you should not rely on the information herein as investment advice. If you are seeking personalized investment advice, please contact a qualified and registered broker, investment adviser, or financial adviser. You should not make any investment decisions based on our communications. Our stock profiles are intended to highlight certain companies for YOUR further investigation; they are NOT recommendations. The securities issued by the companies we profile should be considered high risk and, if you do invest, you may lose your entire investment. Please do your research before investing, including reading the companies’ public filings, press releases, and risk disclosures. Information contained in this profile was provided by the company, and extracted from public filings, company websites, and other publicly available sources. We believe the sources and information are accurate and reliable but we cannot guarantee it. The commentary and opinions in this article are our own, so please do your research.

Copyright © 2024 Micro Math Capital, All rights reserved.