Perion Network is facing one of its greatest tests to date. The digital advertiser lost a key component of its business and Wall Street is punishing them.

We first wrote about Perion after the stock fell 40%, to $12.50, in April 2024. At the time, the company looked cheap and the market’s reaction seemed slightly irrational given the durability of its business model and financial robustness.

However, Perion suffered a major setback when it announced in mid-June that Microsoft, its #1 customer, planned to exclude it, and several partners, from its search distribution marketplace. This was detrimental to Perion because it was expected to cut revenue and profits substantially in 2024.

Following the announcement, Microsoft’s search advertising platform would account for less than 5% of revenue; compared to 34% of revenue in 2023 ($247 million).

By any measure, Perion was being punished and the market was responding accordingly. The stock fell another 34% on the news, and the business has been trading around $8.60 per share at a market cap of $423 million.

The good thing is that this creates a tremendous opportunity.

What Wall Street failed to consider was that Perion Network was diversifying and expanding. In several ways, the Microsoft partnership was an anticipated risk, and management was preparing for the shift by investing heavily in markets outside of its search advertising domain.

These efforts are expected to improve its intrinsic value over the long run while enhancing its business fundamentals immediately. Now, it is time to see what makes this potential investment attractive.

In this article, we highlight the diversity of Perion Network’s business and outline several valuation approaches demonstrating how it appears mispriced by the market.

Under these assumptions, we are doubling down on Perion Network’s long-term investment prospects. Here’s why…

A Quick Overview of Perion Network

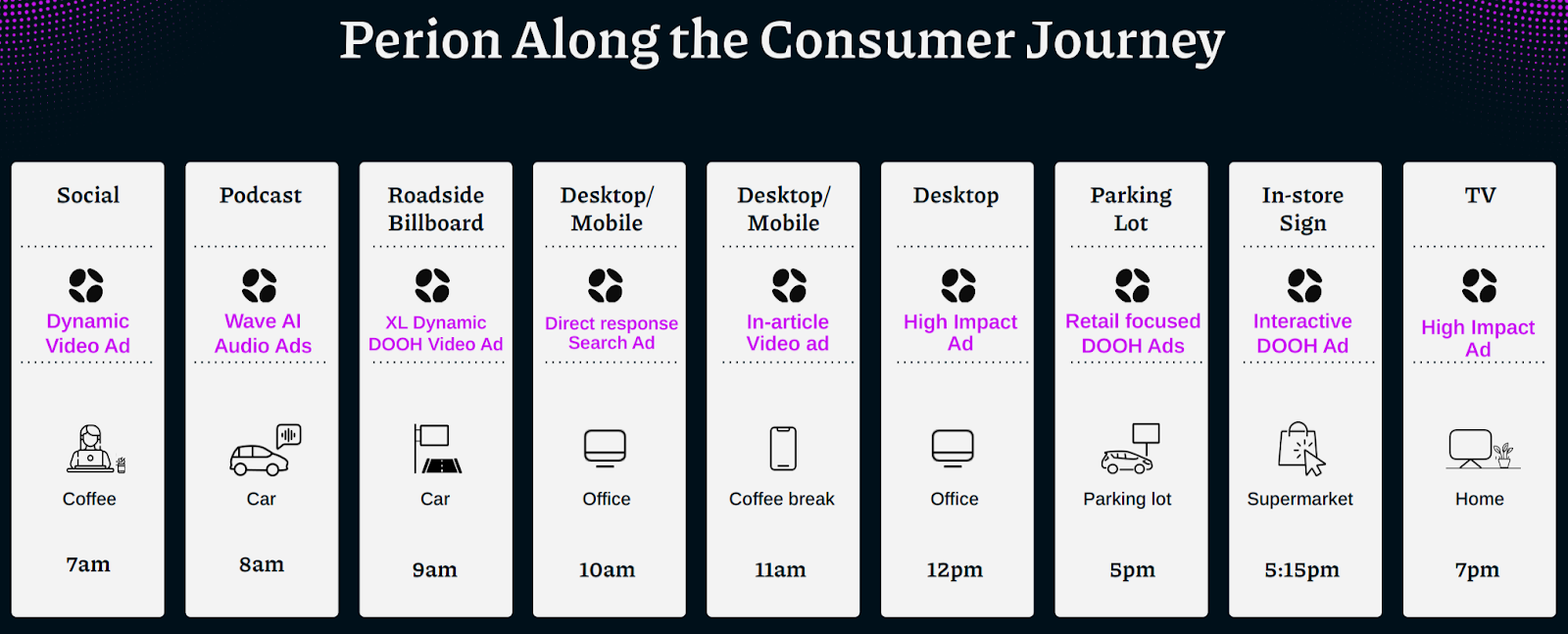

Perion Network is an ad tech company with a two-pronged business model: search advertising and advertising solutions. One of its primary objectives is to help advertisers connect with people at several stages of the consumer journey.

Search Advertising

The company’s search advertising business operates like Google AdSense connecting advertisers to suppliers with a comprehensive and fully customizable solution that delivers maximum exposure and enhanced engagement.

This offering has attracted a variety of premium publishers including Fortune, Nasdaq, Benzinga, Business Insider, LG, and HuffPost, among others. Perion coordinates with these publishers to distribute relevant ads without jeopardizing the user experience.

In 2023, search advertising accounted for 46% ($344.9 million) of the company’s revenue while in Q2 2024 it fell to 32% ($34 million). As of the second quarter, Perion worked with 95 search publishers (-40% YoY) while achieving 16.3 million Average Daily Searches (+20% YoY).

Keep in mind that there may be more heartache in the future as the company reduces its reach on Microsoft Bing. Though this is projected to be a significant loss, Perion continues to operate on Yahoo, YouTube, and every major social media platform.

There are still opportunities to capitalize and generate exposure in this space, however, it is unclear what this market will look like moving forward.

Advertising Solutions

Despite losing a key piece of its business, Perion continues to see strong growth in the second half of its operations.

Through its advertising solutions unit, the company has developed and acquired a series of leading advertising platforms and cutting-edge AI solutions. This accounted for $398.2 million (54%) of the company’s revenue in 2023 and $74.4 million (68%) in Q2 2024 while growing 23% annually since 2021–advertising solutions fell 25% YoY in Q1 2024.

Here is a list of Perion Network’s offerings:

1. Connected TV (CTV) Advertising

The company took a huge leap into the CTV market bridging the gap between traditional cable networks and modernized streaming platforms.

Its CTV solution suite allows publishers to leverage a variety of formats including QR codes, polls, games, and more to reach targetted audiences. This is connected to big-time networks and platforms like CBS, ABC, FOX, and Paramount, among others!

In Q2 2024, CTV advertising grew 42% YoY to $8.2 million (14% of advertising solutions revenue). According to eMarketer, CTV ad spending is expected to grow 72.4% to $42.4 billion in 2027, representing 10% of total digital ad spend in the US.

2. Digital Out-Of-Home (DOOH) Advertising

Another key area of growth for Perion is its DOOH solutions. In 2023, the company acquired Hivestack, a leading DOOH organization for $100 million with access to more than 32 countries; including a recent partnership with Eletromidia Brazil, an OOH media company reaching more than 29 million people daily through over 64,000 DOOH screens.

Perion’s DOOH platform is built to streamline operations and efficiently manage ads for distributors and advertisers. For example, the company’s campaign with Lululemon helped the retailer increase its brand image by 640%, interest by 208%, and footfall traffic by 314% while adding 4,296 incremental walk-ins.

In Q2 2024, DOOH advertising grew 41% YoY to $13.0 million (18% of advertising solutions revenue). According to PQ Media, worldwide DOOH ad spending is expected to grow 42.8% to $30.7 billion in 2026.

3. Open Web Video

One area that has been on the decline recently is Perion’s open web video unit. The company’s solutions enable advertisers to create and show customized ads with audio to attract consumer’s attention while scrolling the web.

In the second quarter of 2024, revenue declined 66% YoY, representing 18% of sales in advertising solutions, compared to 44% in 2023. The company’s video solutions are a lower-margin business and thus management has shifted its attention toward display solutions with higher yields.

Maoz Sigron, Perion’s COO expects this area to stabilize around 15% of sales in the unit moving forward.

4. Perion Network’s Proprietary AI Technology

Alongside Perion’s advertising solutions, the company has built two AI tools to further enhance its capabilities.

SORT 2.0 is Perion’s AI-based audience segmentation solution enabling advertisers to reach customers with targeted ads without invading their data and privacy. The technology analyzes all of the non-PII (Personally Identifiable Information) signals present when someone lands in the company’s network, immediately classifies them into their most likely intent group, and serves them a highly relevant ad.

The other is WAVE, an AI-driven audio advertising solution that creates personalized messages on all digital audio streaming services. The company claims that the technology can adapt in real-time using a variety of factors like context, behavior, geography, and demographics, leading to greater engagement and impact from customers.

Together, these tools have attracted a variety of brands including PepBoys, Stop & Shop, Boar’s Head, and Albertsons, among others. However, it is the entire suite of advertising solutions that make Perion’s business model so compelling.

What is Perion Network Worth?

The loss of Microsoft as a partner was a major setback for Perion Network. However, there are plenty of reasons to believe that the stock remains undervalued and well-positioned for the future.

Conventional Valuation Metrics

Before we dive into the realm of forecasts, let’s take a look at a variety of conventional metrics to assess how Perion compares to its current market valuation:

- P/E (TTM) = 5.62

- Forward P/E = 7.24

- P/S (TTM) = 0.61

- P/B = 0.56

One ratio to highlight is the company’s price-to-book (P/B), a ratio made famous by Benjamin Graham to assess the valuation of a business. Book value or shareholder equity is the remaining value of the business awarded to shareholders if the company was fully liquidated to pay off those it was indebted to.

With $726.0 million in shareholder equity, Perion is trading at a significant discount to its book value given its current market cap of $422.6 million (42% margin of safety). Even if one were to write off all of the company’s goodwill ($332.9 million), a subjective metric that measures the intangible value of its brands and technology, the company would still look attractive at a P/B of just 1.08.

By all conventional accounts, Perion Network looks cheap.

DCF Based on Perion’s Guidance

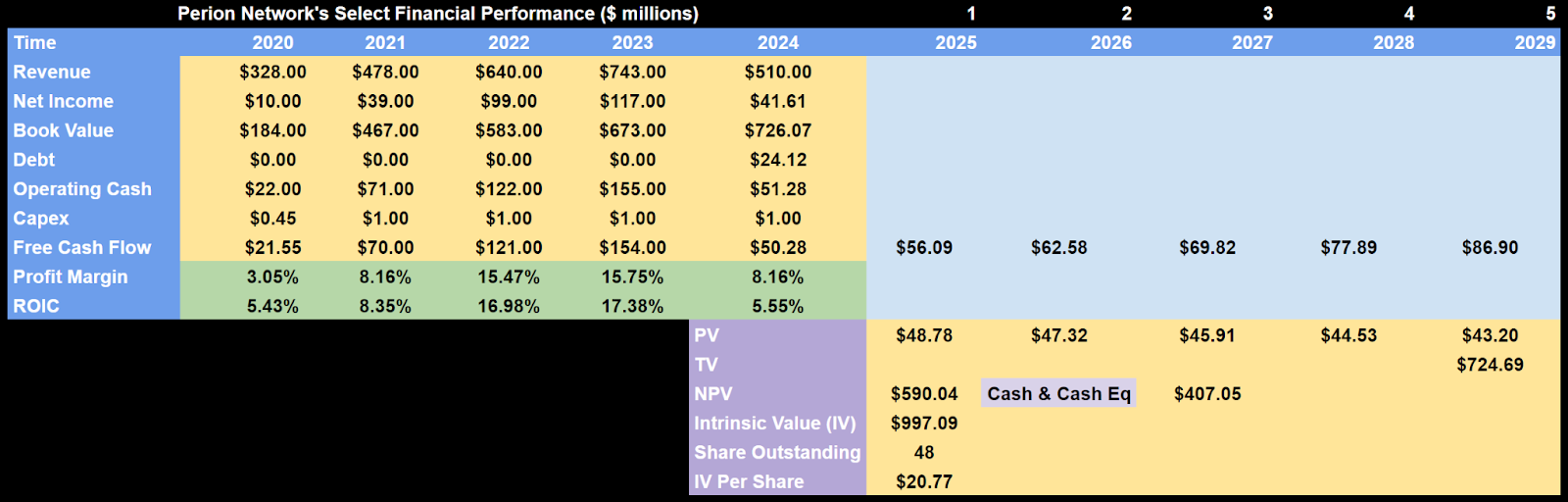

Since Perion has outlined revenue ($490 to $510 million) and EBITDA ($48 to $52 million) guidance for 2024, we can leverage these numbers and calculate an intrinsic value using a discounted cash flow model.

To keep our valuations conservative, the DCF models use a discount rate of 15% throughout.

On the high end of guidance, the model determined that Perion is worth $997.1 million at $20.77 per share. This implies that the company currently trades at a margin of safety of 57.58%.

For this model, Perion’s future cash flows were projected to grow using a historical growth rate of 12.04% over five years and a terminal growth rate of 3.01%.

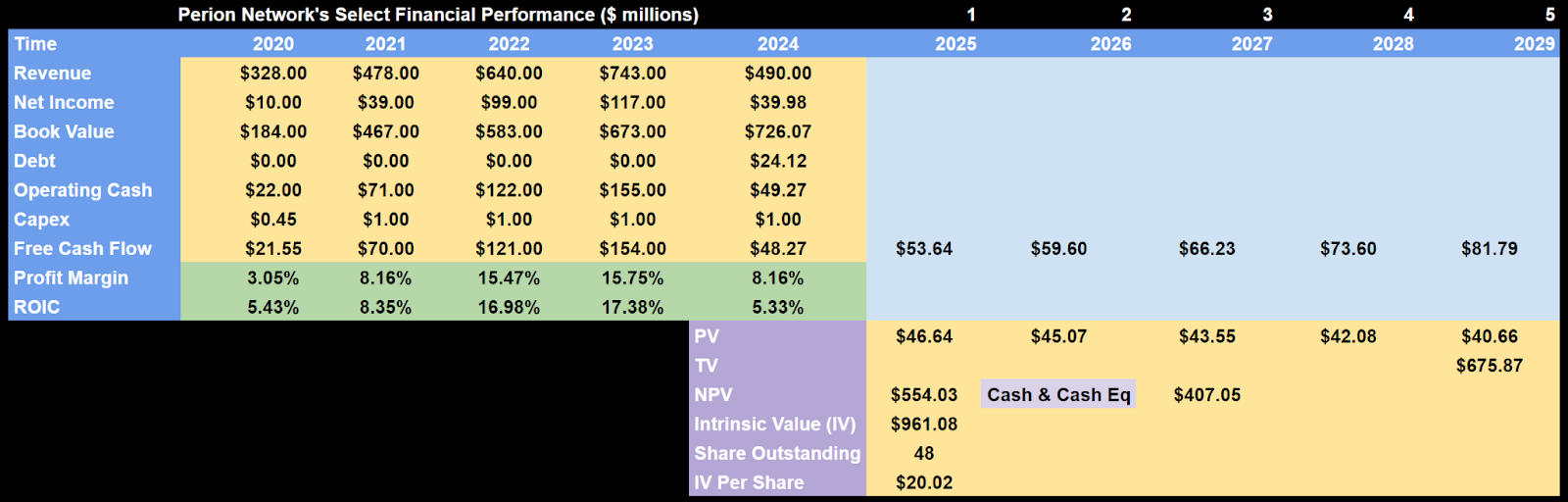

On the low end of guidance, the model determined that Perion Network is worth $961.1 million at $20.02 per share. This implies that the company currently trades at a margin of safety of 55.99%.

For this model, Perion’s future cash flows were projected to grow using a historical growth rate of 11.59% over five years and a terminal growth rate of 2.90%.

Doomsday DCF

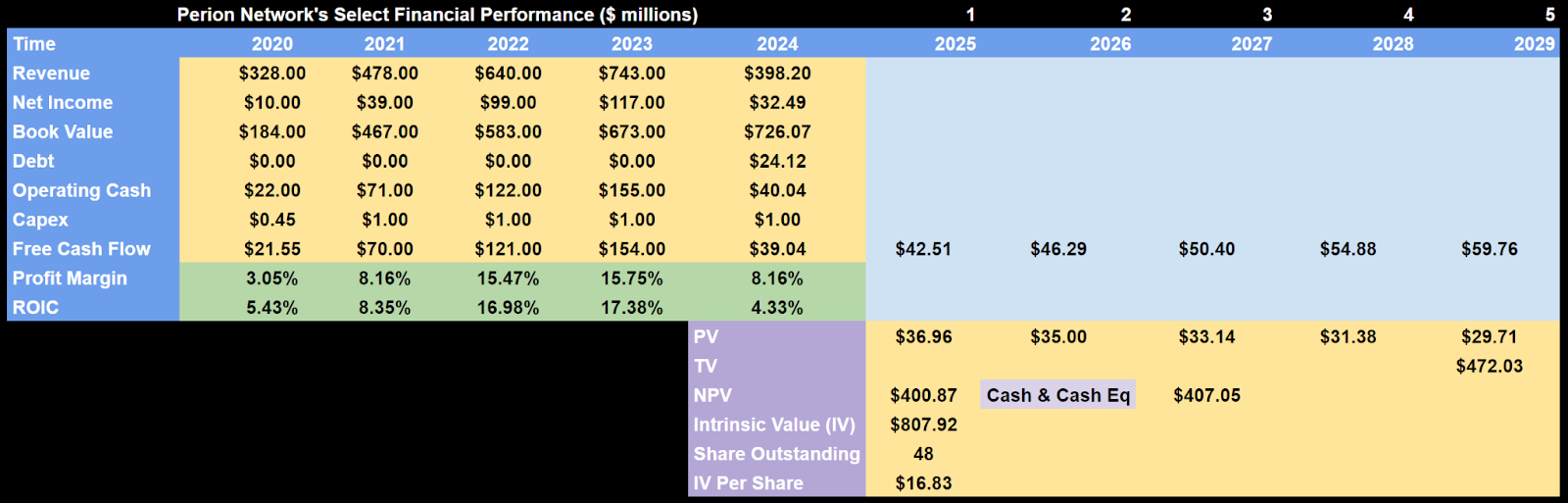

To make things interesting, let’s imagine that Perion’s search advertising business is a complete bust. In this hypothetical scenario, there is no longer any demand for this unit and Perion must rely entirely on its advertising solutions segment.

Using Perion’s revenue from last year, with no consideration for growth year-over-year, we can determine what the company would be worth if it slashed another $100 million in sales from its business. Here are the results…

In our doomsday scenario, the model determined that Perion Network is worth $807.9 million at $16.83 per share. This implies that the company currently trades at an implied margin of safety of 47.64%.

For this model, Perion’s future cash flows were projected to grow using a historical compound annual growth rate of 9.36% over five years and a terminal growth rate of 2.34%.

Final Thoughts

Perion Network may be punished temporarily, but its future looks promising. The company operates with little debt, ample cash, and a diversified business model that continues to grow.

Though the market is disappointed by the recent news and the end of a fruitful relationship with Microsoft, there are plenty of opportunities for Perion to capitalize elsewhere. The bandaid has been figuratively ripped off and now the company can focus on the next phase of its development.

That is not to say that Perion won’t experience pain from this disruption, but rather that its fundamentals appear resilient enough to endure any short-term setbacks. Management seems to second this belief as they continue to “execute [their] $75 million buyback program” and “strongly believe that [their] publicly traded shares are significantly undervalued” despite expecting to miss out on substantial earnings throughout the remainder of 2024.

With the stock appearing to trade below what the business is worth and a large margin of safety protecting its downside risk, Perion Network looks to be one of the most attractive opportunities in the market today. The company will need to demonstrate that it can overcome these setbacks, but we are optimistic that it can turn things around.

Disclosure

We are not brokers, investment, or financial advisers, and you should not rely on the information herein as investment advice. If you are seeking personalized investment advice, please contact a qualified and registered broker, investment adviser, or financial adviser. You should not make any investment decisions based on our communications. Our stock profiles are intended to highlight certain companies for YOUR further investigation; they are NOT recommendations. The securities issued by the companies we profile should be considered high risk and, if you do invest, you may lose your entire investment. One or more Micro Math Capital employees own shares in Perion Network. Please do your research before investing, including reading the companies’ public filings, press releases, and risk disclosures. Information contained in this profile was provided by the company, and extracted from public filings, company websites, and other publicly available sources. We believe the sources and information are accurate and reliable but we cannot guarantee it. The commentary and opinions in this article are our own, so please do your research.

Copyright © 2024 Micro Math Capital, All rights reserved.