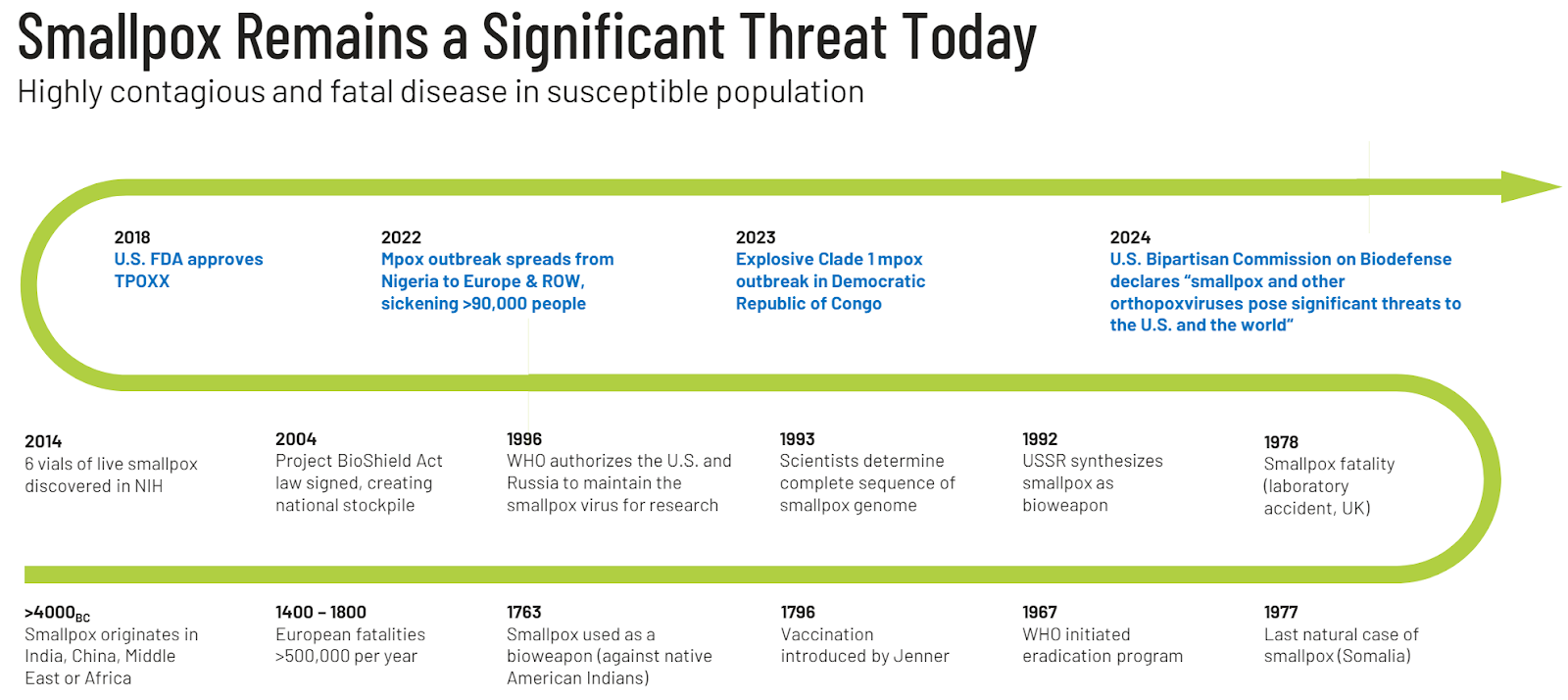

Smallpox is one of the deadliest diseases known to humankind. It killed more than 300 million people in the 20th century alone, possessing a 30% mortality rate when contracted.

Though its origins are debatable, smallpox outbreaks have existed for more than 3,000 years, appearing in places like India, Egypt, and China. Victims of the virus experience a range of irritating symptoms including fevers, vomiting, skin rashes, and severe back pain while 65 to 80% of survivors are marked with deep pitted scars (pockmarks), most prominent on the face.

Due to its devastation, the World Health Organization (WHO) launched an intensified plan, in 1967, to annihilate smallpox once and for all. This became one of the most successful collaborative public health initiatives in history as the disease was declared globally eradicated by 1979.

Or so we thought.

As it stands, governments around the world are quietly building up stockpiles of smallpox vaccines. With the threat of biological warfare expanding and the effects of COVID-19 lingering, state leaders are taking measures to prevent the next outbreak. If it happens to be smallpox, the goal is to cut it off before it devastates the world.

That is how our topic company manages to produce a 78% gross margin and 49% net profit margin on $157 million in sales from a virus posing no immediate threat. The stock trades at a market cap of $543.55 million and a P/E of just 6.95 demonstrating a massive potential for growth moving forward.

The question is whether it can sustain itself by developing treatments for a disease that has been dormant for more than 40 years. Let’s find out.

Understanding SIGA Technologies

SIGA Technologies (SIGA) is a commercial-stage pharmaceutical company whose primary offering, TPOXX, is an anti-viral treatment built to eliminate smallpox and other orthopoxviruses (i.e. monkeypox, cowpox, and the vaccinia virus).

The oral and IV-administered drug has been FDA-approved since 2018 and is now sold in more than 25 countries. Additionally, TPOXX is approved for treating orthopox by the EMA (European Medicines Agency), making it one of two available antivirals serving this market.

To manufacture and distribute the treatment, SIGA has built a fully integrated, US-based operational supply chain that includes partners like Pfizer and Catalent. This allows it to effectively scale its production to meet the needs of its customers.

Speaking of demand, SIGA primarily serves government entities both in the US and abroad.

For example:

- SIGA’s first US contract came from the US Biomedical Advanced Research and Development Authority (BARDA) for $461 million of total procurement over eight years (2011-2018). The company then renewed its contract in 2018, adding $536 million worth of TPOXX deliveries to its pipeline; so far, SIGA completed $408 million of orders with another $138 million set for delivery soon.

- SIGA is targeting a contract with the Administration for Strategic Preparedness & Response (ASPR) for the U.S. National Stockpile this year.

- SIGA been working with the US Department of Defense (DoD) to develop a Post Exposure Prophylaxis (PEP) indication for TPOXX ($27 million in funding) while fulfilling stockpile demands as well (The DoD purchased up to $18.1 Million of Oral TPOXX in 2022).

- Lastly, SIGA has made extensive efforts to diversify its business outside the United States. The company signed an $18 million deal with 13 members of the European Union, in 2023, and recently announced an agreement to sell TPOXX to ASEAN member states. These are just a few of the international markets it serves.

Overall, SIGA remains highly dependent on the US market, but global investments are proving to be an effective cash generator for the company long term. Furthermore, the company is exploring novel TPOXX formulations and indications to bolster its expansion efforts. The combination of a fruitful US market, growth opportunities abroad, and new treatment opportunities position SIGA Technologies well.

Why is SIGA Technologies Different?

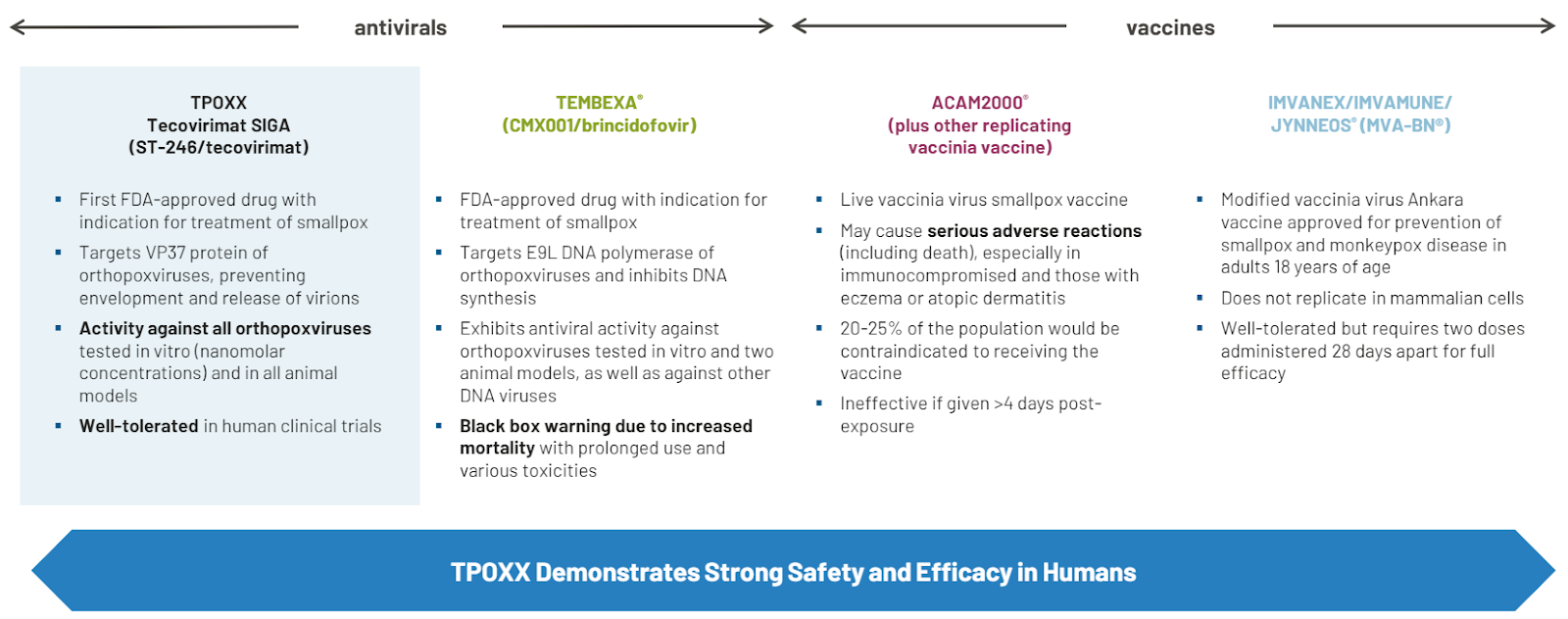

There are just four clinically approved medications for treating smallpox and orthopox viruses. But as you can see, TPOXX is the most effective solution based on efficacy, versatility, and safety.

From a design standpoint, TPOXX prevents the virus from further development, is effective on several variations of the orthopox virus, and is generally safe for humans. While other treatments provide some degree of therapy, they contain one or several defects that prohibit them from being a reliable solution.

This gives SIGA a technical advantage that is difficult to replicate. With a better/safer product, customers are more likely to choose their offering over competing alternatives.

However, this does not guarantee success. What truly separates SIGA Technologies is its distribution capabilities and government relations experience.

Through its fully integrated supply chain network, the company can easily scale its production capabilities to whatever the market demands. This is critical because it means that there is limited risk of a shortage which otherwise has a severe impact on sales and its relationship with customers; Novo Nordisk is a prime example.

More importantly, SIGA has developed strong ties with government entities around the world. By having these connections and efficiently resolving regulatory constraints, the company has quickly penetrated international markets on multiple continents.

In all, SIGA’s technical expertise, economies of scale, and strong relationship with governments make it the clear-cut winner in the smallpox market.

SIGA’s Leadership

One area where SIGA is less attractive is its management team. At the beginning of 2024 and late 2023, the company appointed a new CEO, Dr. Diem Nguyen to replace Dr. Phil Gomez, who was retiring, and named Dr, Jay K. Varma as its new Executive Vice President and Chief Medical Officer.

Both doctors are qualified professionals who are expected to excel in their new positions. Dr. Nguyen is an experienced executive who has played key roles at several biotech firms, including Global President at Pfizer. Dr. Varma on the other hand was directly recruited by the Mayor of New York to serve as the principal scientific spokesperson and architect for the city’s COVID-19 pandemic response.

However, there are concerns that SIGA’s culture could change now that its executive team is reorganizing and the old guard is on its way out. With new leaders, it is difficult to predict whether this will improve the business or hinder it. Since SIGA has achieved tremendous success as of late, it is possible that things could turn for the worse now that someone new is spearheading their strategic direction.

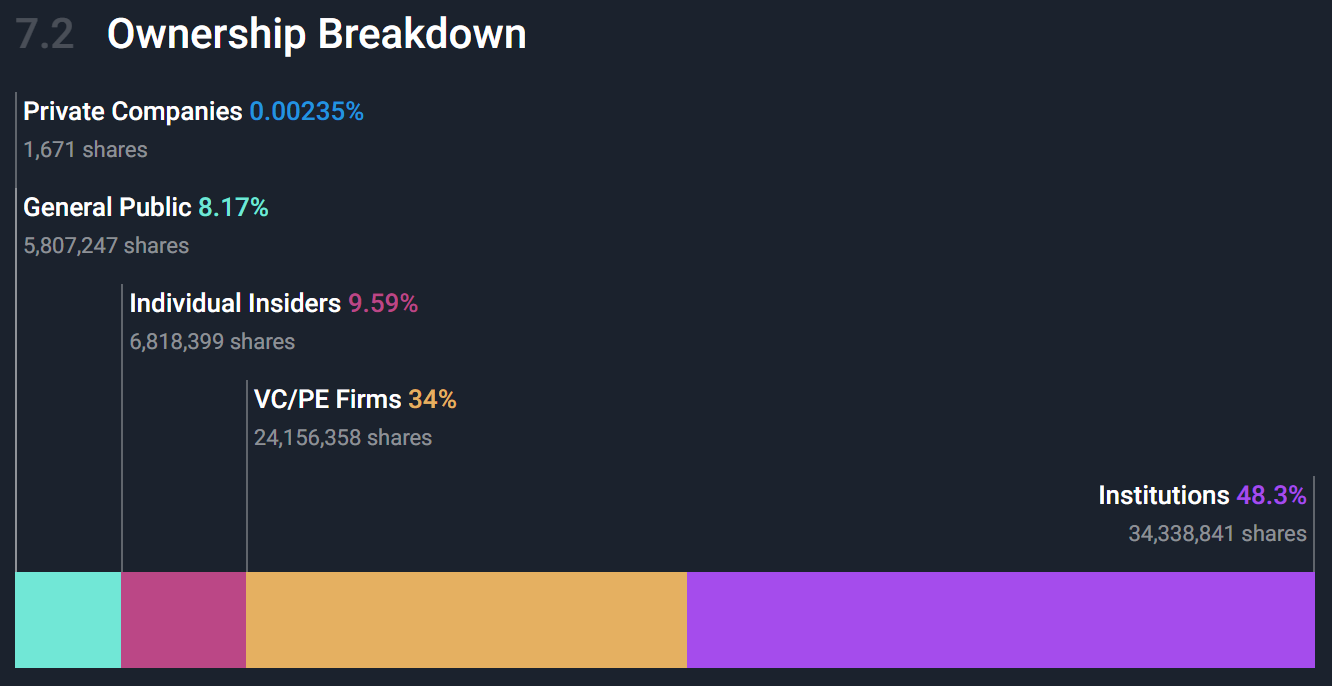

Additionally, it is problematic that these new execs lack skin in the game. Without the majority of their capital tied to the company, there is a risk that management will fail to act in shareholders’ best interests because there is no risk to themselves.

To be fair, Simply Wall Street outlines that SIGA insiders own roughly 9.59% of the company’s common shares. This gives us confidence that even though the new executives may lack capital investment, there is enough at stake so that its board and other executives can hold the new leaders accountable.

Ultimately, it is yet to be determined whether this new leadership can deliver and elevate SIGA’s position in the marketplace. Only time will tell.

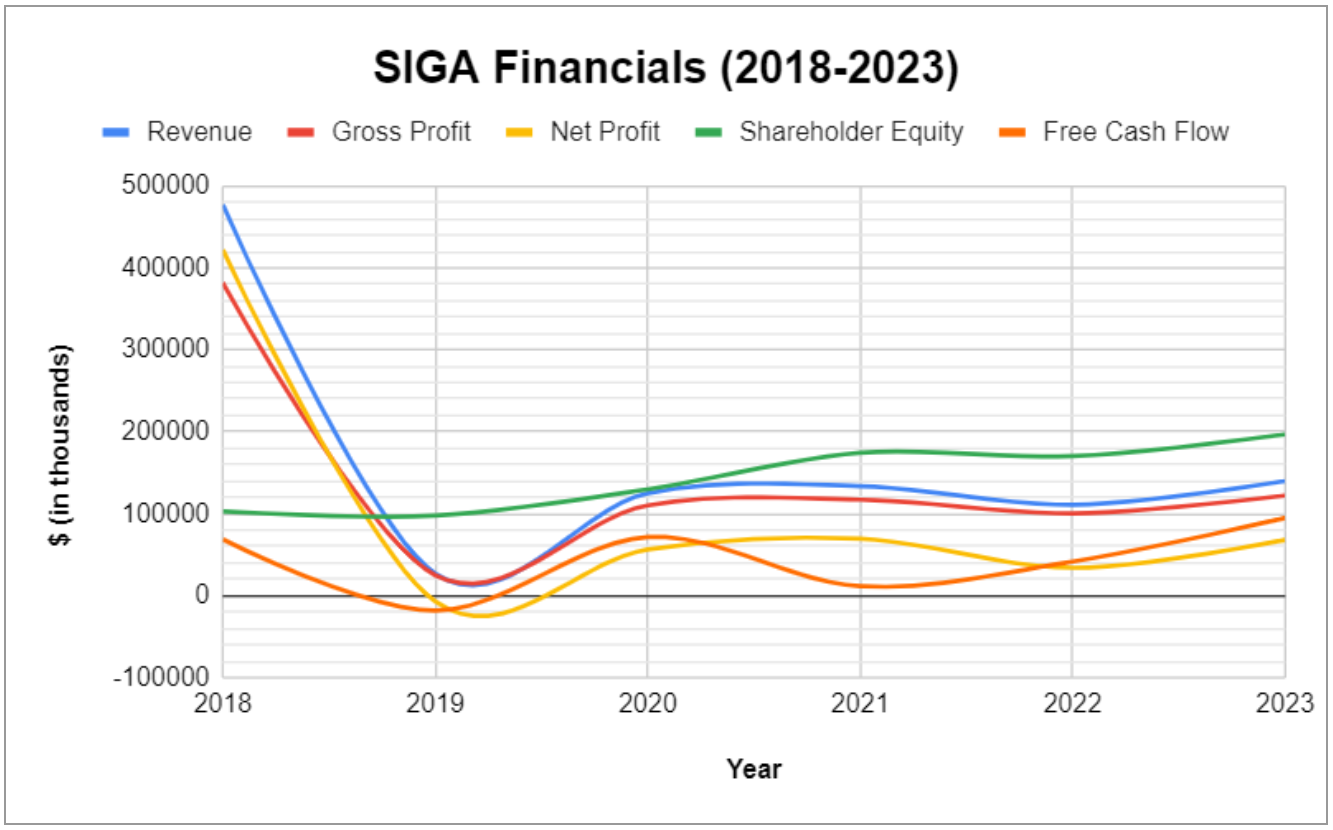

SIGA’s Financials

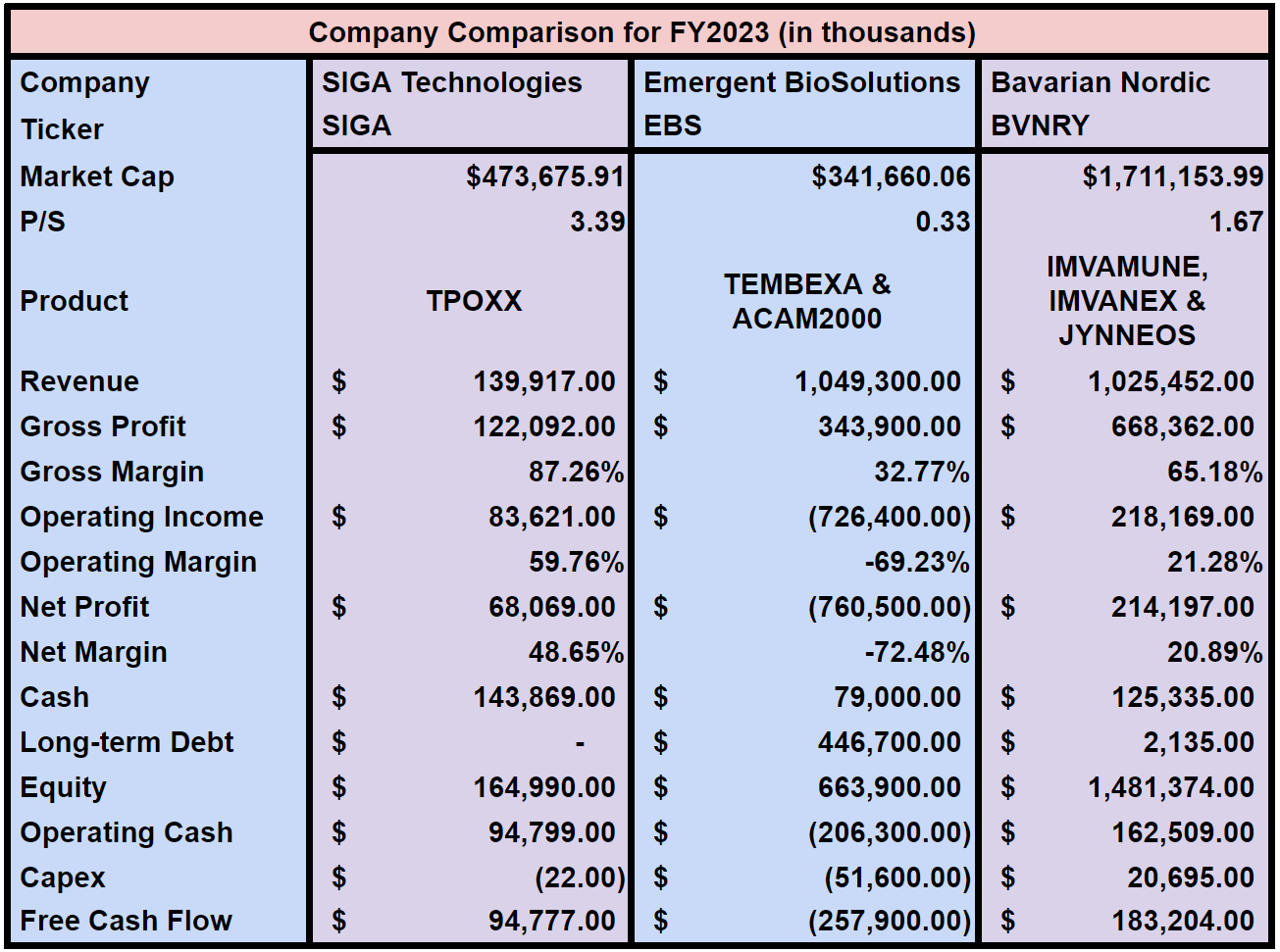

The primary reason SIGA Technologies caught our attention was due to its exceptional financial characteristics. From a 78% gross margin to over $94 million in annual free cash flow and zero debt, there is a lot to like about the company.

Moreover, when you compare SIGA to its competitors, it clearly stands as the better business: higher gross margin, operating margin, net profit margin, more cash, less debt, etc.

However, when analyzing SIGA’s financial track record, it becomes apparent that the business’s performance tends to fluctuate from year to year, making it less predictable than we would typically prefer.

More importantly, it highlights weaknesses in the company’s current business model.

For one, SIGA remains primarily dependent on the US market. Over the past four years (2020 to 2023), 79% of its revenue came from the US. Though the company has invested heavily in its international pipeline, the reality is that SIGA needs the US economy to thrive. Without it, the company will be a fraction of what it is today.

Second, SIGA receives its payments in lump sums which makes the business less predictable. 2018 is a prime example as the company recorded all of its revenue from one BARDA contract. On the other hand, 2022 demonstrates how a lack of contracts/orders leads to a meaningful impact on its earnings as net profits fell from $69.5 million to $33.9 million in a single year.

Fortunately, SIGA’s expansion abroad has helped stabilize its annual financial performance, as the number of TPOXX orders increases. However, this continues to be a sizeable risk that limits the company’s ability to invest from one year to the next.

Which brings us to our last point. There is a cap on the number of TPOXX vaccines a country requires in a given period. Since the virus poses a limited threat at this time, SIGA’s customers can only demand so much.

Yes, the company can expand outward to other countries, but it can not increase its production within a specific market. This forces SIGA to wait for its customer’s treatments to expire before it can replenish its stockpile; according to the FDA, TPOXX has a shelf-life of 3.5 years.

Overall, SIGA remains a financially robust business, but one must be cognizant of its inherent weaknesses. With no other product on the market, the company is fully dependent on governments continuing their smallpox programs to succeed.

Points of Criticism

Throughout the article, we have highlighted areas of SIGA that may cause you to question its investment prospects. Here is a quick summary of those points to help you recall areas of weakness in the business:

- New Management, No Skin in the Game: key executives joined SIGA less than a year ago and lack capital investment in the company.

- US-Market Dependency: The US made up 79% of its revenue over the past four years (2020-2023).

- Lump-sum Payments: SIGA receives lump-sum payments that make its financials less predictable.

- Cap on Demand within a given Market: Governments require a set amount of TPOXX in a given period, preventing excess growth.

Final Thoughts

There is a lot to like about SIGA Technologies. On paper, its financial characteristics are exceptional and its competitive positioning is unmatched, making it a highly attractive investment overall.

That being said, SIGA’s success largely depends on governments believing that smallpox is a worthy threat to their citizens. The company can only profit in this market for so long before new solutions emerge or a more serious threat arises.

This forces the company to continue expanding or seek out new treatments if they wish to survive. Otherwise, it may back itself into a situation with no room to escape.

There is a caveat to this argument, however. If a smallpox outbreak were to occur, SIGA would receive exponential demand that would elevate its valuation far beyond what it is today.

The question is whether you are willing to own a company that is banking on an endemic that may never come.

Disclaimer/Disclosure:

We are not brokers, investment, or financial advisers, and you should not rely on the information herein as investment advice. If you are seeking personalized investment advice, please contact a qualified and registered broker, investment adviser, or financial adviser. You should not make any investment decisions based on our communications. Our stock profiles are intended to highlight certain companies for YOUR further investigation; they are NOT recommendations. The securities issued by the companies we profile should be considered high risk and, if you do invest, you may lose your entire investment. Please do your research before investing, including reading the companies’ public filings, press releases, and risk disclosures. Information contained in this profile was provided by the company, and extracted from public filings, company websites, and other publicly available sources. We believe the sources and information are accurate and reliable but we cannot guarantee it. The commentary and opinions in this article are our own, so please do your research.

Copyright © 2024 Micro Math Capital, All rights reserved.