Gold has long been hailed as the “Metal of Kings”. Since the days of the ancient Egyptians, it has weathered the storms of wars, disasters, and the collapse of entire civilizations.

In each era, gold has stood firm, maintaining and appreciating its value, acting as a reliable store of wealth, a hedge against inflation, and a haven during times of economic turmoil. Today, in an era marked by geopolitical tension and financial instability, its role is more vital than ever.

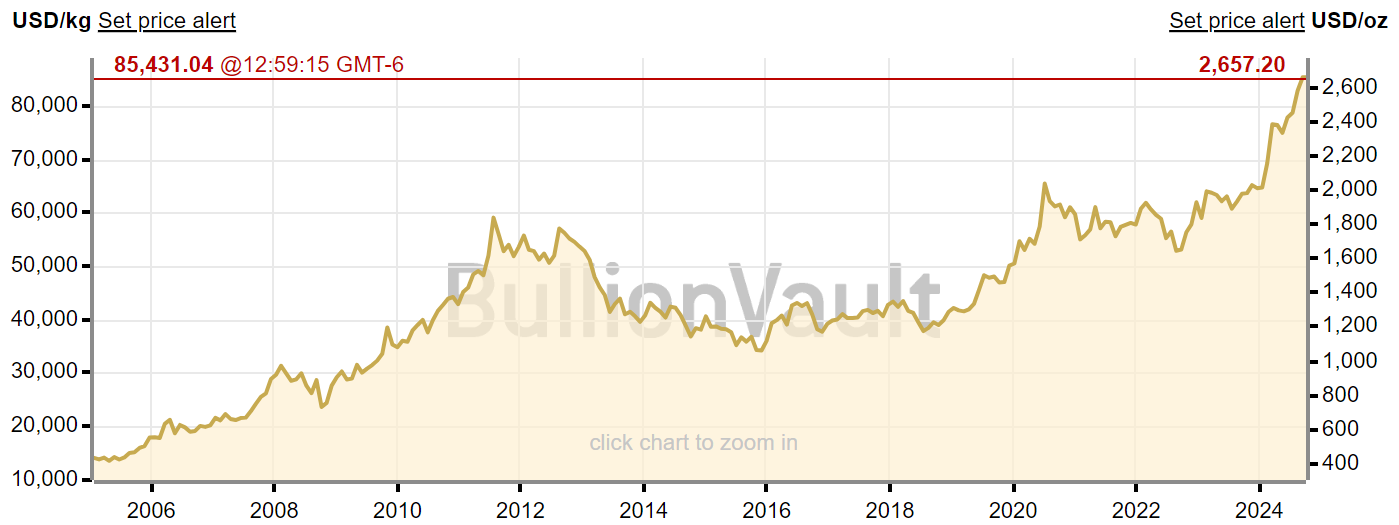

With gold trading at an all-time high and surging 37.07% in the last year alone, it’s no surprise that governments, investors, and even everyday citizens are turning to this precious metal as a shield against a looming global economic downturn. The reckless expansion of government debt, coupled with the weakening of major currencies like the US dollar, has pushed many to seek refuge in an asset that offers stability, security, and confidence in the face of political and financial uncertainty.

But as gold prices soar, what’s the best way to capitalize on this momentum?

Sure, you could invest in physical gold, but with storage costs, space limitations, and prices at historic highs, it might not be the most practical choice. Alternatively, you could look to large gold miners like Barrick Gold, Newmont, or Agnico Eagle, whose stock valuations have soared alongside gold’s rally.

However, we believe there’s an even more compelling opportunity on the horizon: a Canadian junior mining company with a significant gold discovery in mining-friendly Ontario. This under-the-radar company has unearthed a gold deposit that rivals those of much larger competitors, yet it remains undervalued compared to other junior miners in the region. In fact, the company has quickly tripled the size of its land holdings, positioning itself to uncover even more lucrative deposits.

Here’s where it gets interesting: you have the chance to invest in this company before it hits the mainstream. With proven reserves and enormous untapped potential, this junior miner has caught the attention of major industry players, and it should be on your radar, too. This is a rare ground-floor opportunity to get in early before the market fully recognizes its value.

So without further ado, it’s time to explore Delta Resources (TSXV: DLTA) (OTCBB: DTARF).

What is Delta Resources?

Delta Resources is rapidly emerging as a significant player in the gold exploration space, particularly with its Delta-1 project, located just 50 km west of Thunder Bay, Ontario. This project sits in the Shebandowan Greenstone Belt—a region renowned for its rich deposits of gold, copper, and nickel. The area has long attracted interest from major players, most notably Inco Limited which operated the nearby Shebandowan Cu-Ni-PGE mine from 1972 to 1998, extracting millions of tonnes of high-grade ore. But there was always a suspicion that the region held more—a hidden gold potential that has gone largely untapped.

Fast forward to today, and Delta Resources is picking up where the industry left off, setting its sights on unlocking this hidden wealth.

In the late ’80s and early ’90s, Inco’s subsidiary, Inco Gold, conducted early-stage exploration in the Shebandowan Belt. They drilled promising intercepts, including 3.28 g/t gold over 14.6 meters in the I-Zone, 0.7 g/t Au over 39 meters in the South Zone, and 44.5 g/t Au from a grab sample in the Kukkee Occurrence. Despite these promising signs, the project was abandoned when Inco Gold merged with Consolidated TVX.

From there (1995 to 1997), Landore Resources picked up where Inco Gold left-off, reporting highlight drill intercepts of 4.32 g/t Au over 41m, 4.53 g/t Au over 14.4m and 4.36 g/t Au over 20.4m, in the I-Zone. Mengold Resources also conducted research on the property, in 2008, finding grades as high as 293.2 g/t gold and 1090 g/t silver in the South Zone. Yet, the area has remained vastly underexplored—until Delta Resources entered the picture.

Delta began acquiring land in the region in 2019, and by early 2020, their initial exploratory drill program revealed a wide zone of economic-grade gold mineralization over a 200-meter strike length in what is now known as the Eureka Gold Deposit. Encouraged by these results, Delta wasted no time expanding its drilling programs. Between 2021 and 2022, their continued efforts uncovered high-grade intercepts such as 5.92 g/t gold over 31 meters, including 14.80 g/t Au over 11.9 meters, and 72.95 g/t Au over 2.2 meters—suggesting that Delta-1 held far greater potential than initially thought.

With these results in hand, Delta Resources doubled down, rapidly expanding its land holdings and intensifying its drilling efforts. In 2023, the company launched two drilling campaigns, totaling an ambitious 25,000 meters. The results were nothing short of impressive, with highlight intercepts including 6.49 g/t gold over 10 meters, 4.23 g/t Au over 26.2 meters, and 2.16 g/t Au over a staggering 97.5 meters. These combined efforts earned them the prestigious 2022 Bernie Schnieders Discovery of the Year Award from the Northwestern Ontario Prospectors Association—a clear signal that Delta-1 is one of the most promising gold discoveries in recent years.

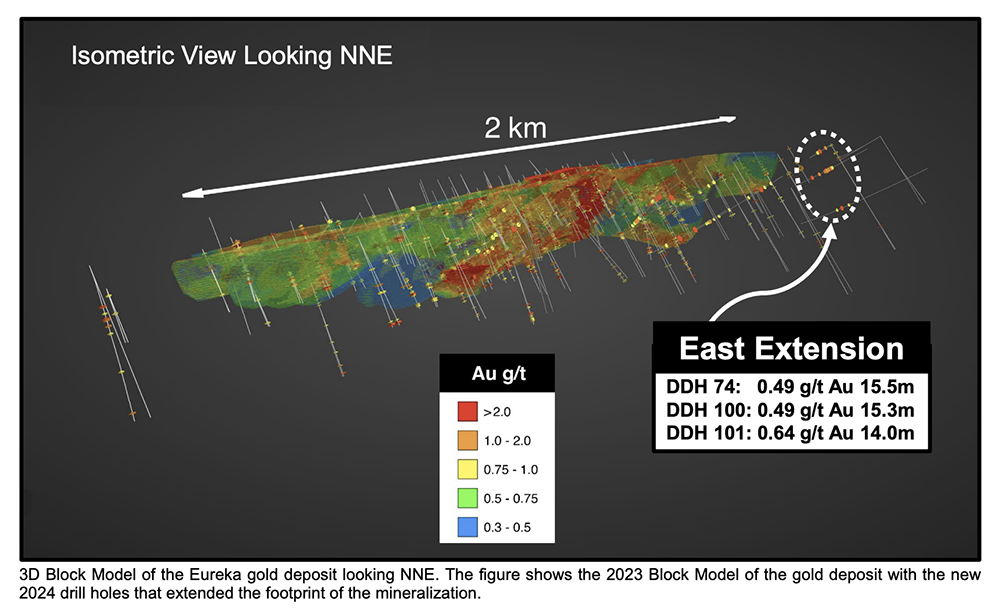

By mid-2024, Delta had drilled an additional 9,286 meters, further reinforcing the project’s resource potential. Standout intercepts from this campaign included 15.94 g/t gold over 10 meters and 1.64 g/t Au over 29.5 meters. What’s more, the Eureka Gold Deposit’s strike length now spans 2.5 kilometers and reaches depths of 300 meters from the surface, with vast areas of the property yet to be explored..

Perhaps even more exciting is Delta’s aggressive expansion of its land position, now commanding an impressive 30,600 hectares (306 square kilometers) of prime exploration ground. Much of this land shares similar geological characteristics with the Eureka Deposit, hinting at the potential for multiple significant gold discoveries across the property.

To date, Delta has drilled 115 holes across 35,575 meters, but they are just scratching the surface. The project’s scale and scope continue to grow, with new deposits expected to emerge in future drilling programs. With its large land position, high-grade intercepts, and growing resource base, Delta Resources is positioning itself to become a major player in Ontario’s gold-rich Shebandowan Greenstone Belt.

Comparing Delta to Goldshore

When evaluating junior mining companies, it’s essential to benchmark them against their peers to get a clearer sense of how their deposits and valuations compare. In the case of Delta Resources, the company sits adjacent to Goldshore Resources (TSXV: GSHR) (OTCQB: GSHRF), a company with a larger market presence but one that shares the same gold-rich Shebandowan Greenstone Belt.

Goldshore’s Moss Lake Gold Project is their crown jewel. Since taking ownership, the company has poured over $60 million into the project, completing nearly 80,000 meters of drilling, building on an additional 155,000 meters completed before Goldshore’s involvement. These extensive efforts culminated in a 2024 updated NI 43-101 resource estimate, showing 1.54 million ounces of Indicated gold resources at 1.23 g/t and a further 5.20 million ounces of Inferred resources at 1.11 g/t, spanning 3.6 kilometers.

Now, let’s compare this with Delta Resources. With a total investment of under $9 million and just 35,000 meters of drilling at its Delta-1 project, Delta is still early in its exploration journey. While they have yet to release an official NI 43-101 mineral resource estimate, the evidence already points to a significant gold accumulation over a 2.5 km long strike, with a surface-to-vertical depth of 300-meters.

Despite the disparity in drilling meters and capital deployed, the valuation difference between these two companies is staggering. Goldshore Resources currently trades at a market cap of $97 million, while Delta Resources is valued at a mere $13.6 million. Both companies are working in the same gold-endowed belt, yet the gap in market value is immense.

Given Delta’s promising results, there’s a compelling case that the company is significantly undervalued. If Delta’s upcoming exploration efforts continue to deliver strong results, there’s every reason to believe its valuation could climb to match or even exceed Goldshore’s. At the very least, the market should recognize Delta’s potential and price it more competitively with its neighbor.

An Underestimated Element of Delta Resources

Developing a mine is an expensive endeavor, requiring careful budgeting for equipment, labor, energy, transportation, environmental compliance, permitting, processing, insurance, and administration costs. Any misstep in managing these can quickly erode a project’s profitability, making even the most promising resource less attractive to develop.

That’s why larger mining companies are always on the lookout for ways to mitigate these costs before taking on new ventures. When evaluating junior mining companies as potential acquisition targets, they’re not just looking for abundant, high-quality resources; they want to ensure that operational friction is kept to a minimum, with infrastructure and logistics in place to support cost-effective development.

This is where Delta Resources stands out. While it’s already clear that Delta’s Delta-1 project has an abundant and high-quality gold deposit, the real hidden value lies in its strategic location.

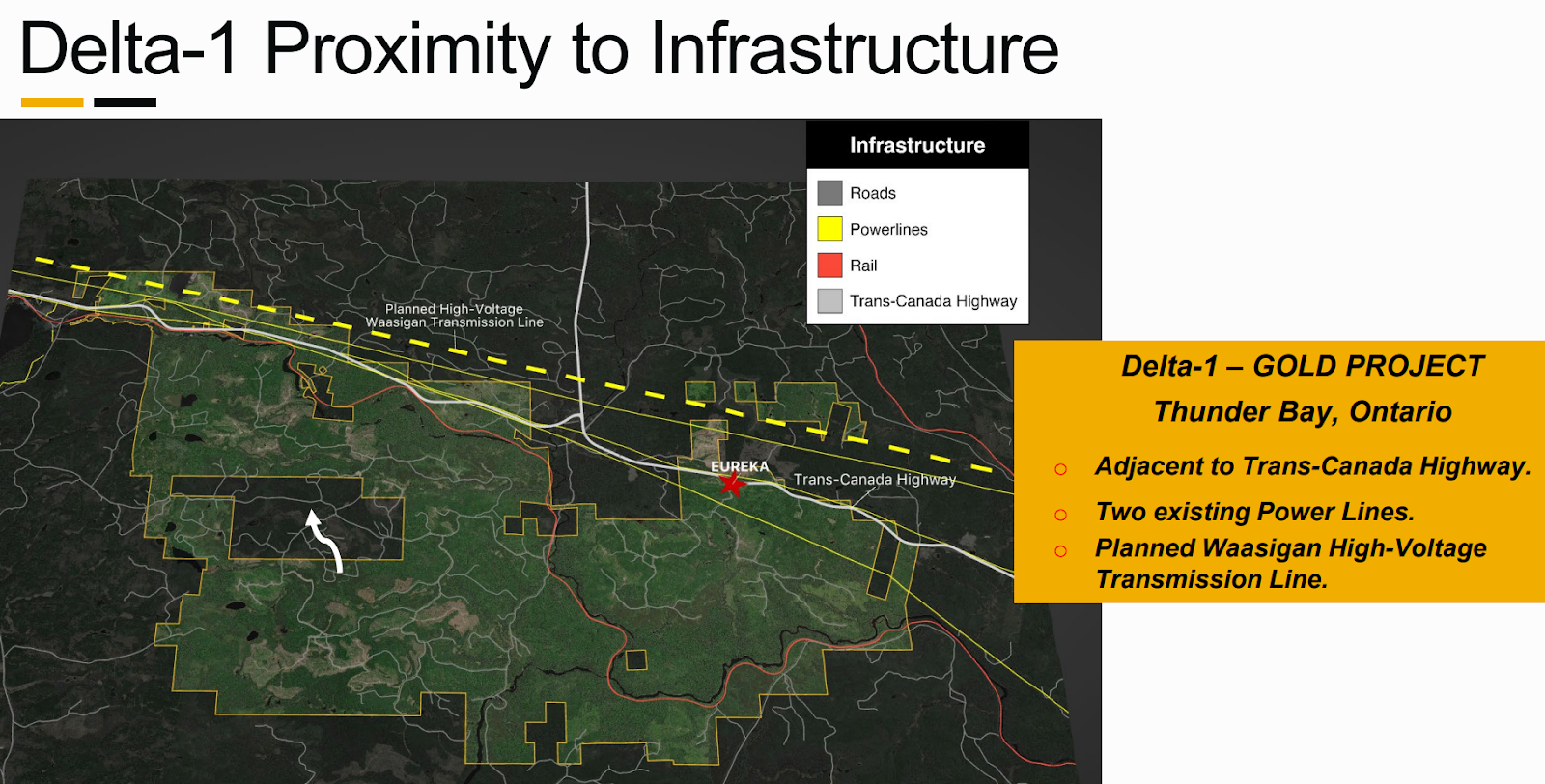

Situated just 50 kilometers west of Thunder Bay, Ontario, the Delta-1 project offers exceptional logistical advantages. Thunder Bay is a major port city with easy access to global distribution channels, allowing for the seamless transportation of gold to international markets. Even more importantly, the project sits adjacent to the Trans-Canada Highway, where robust infrastructure is already in place. Power lines, railway tracks, and year-round road access are all within arm’s reach, significantly reducing the logistical and transportation costs associated with mine development.

For potential acquirers, these advantages make Delta-1 an attractive proposition. Not only is the gold deposit high-grade, but the project’s location allows for operational efficiencies that could lead to outsized returns. By minimizing key expenses like transportation and energy infrastructure, a larger mining company could maximize profits while reducing the usual operational headaches and large capital expenditures that come with remote mining sites.

In short, Delta Resources has positioned itself perfectly, offering not only a resource-rich gold deposit but also the infrastructure to support efficient, cost-effective mining. It’s this combination that could make Delta-1 a highly desirable acquisition for any major player looking to expand its portfolio with minimal friction and maximum return.

Final Thoughts

If you’re looking to seize the moment and profit from the surging demand for gold—driven by geopolitical conflict, economic uncertainty, and the weakening US dollar—Delta Resources (TSX-V: DLTA) (OTCBB: DTARF) should be on your radar.

With a proven, high-grade gold deposit and the added advantage of being strategically located near Thunder Bay, the Trans-Canada Highway, and essential infrastructure, Delta offers a unique investment opportunity with the potential for outsized returns. What makes this even more compelling is Delta’s current undervaluation compared to its mining peers, positioning it as a far more enticing option than companies trading at higher multiples.

While there are many ways to gain exposure to gold, few offer the ground-floor opportunity that Delta Resources does. As it continues to unlock the value of its Delta-1 project, investors could see a significant upside in the near future.

To learn more about Delta Resources and its flagship Delta-1 project, visit deltaresources.ca.

Disclosure/Disclaimer:

We are not brokers, investment, or financial advisers; you should not rely on the information herein as investment advice. If you are seeking personalized investment advice, please contact a qualified and registered broker, investment adviser, or financial adviser. You should not make any investment decisions based on our communications. Our stock profiles are intended to highlight certain companies for YOUR further investigation; they are NOT recommendations. The securities issued by the companies we profile should be considered high risk and, if you do invest, you may lose your entire investment. Apollo Shareholder Relations and its owners do not currently hold shares in Delta Resources Limited and have been compensated for content creation, amounting to thirty-five thousand five hundred dollars. All content is being sent on behalf of Delta Resources Limited by Apollo Shareholder Relations. Apollo Shareholder Relations and its owners reserve the right to buy and sell shares in Delta Resources Limited without further notice, which may impact the share price. Please do your own research before investing, including reading the companies’ public filings, press releases, and risk disclosures. The company provided information in this profile, extracted from public filings, company websites, and other publicly available sources. We believe the sources and information are accurate and reliable but we cannot guarantee it. The commentary and opinions in this article are our own, so please do your own research.