Short selling is a necessary evil. At its best, the short-seller plays a crucial role in exposing corporate corruption and highlighting the vulnerabilities hidden beneath a company’s shiny exterior.

This type of investigative research serves as a safeguard, helping investors avoid reckless decisions or, at the very least, offering a different perspective on the companies they hold or are considering.

But not all short-sellers have noble intentions. Some target stocks purely for personal gain, with little concern for the potential damage they cause to the businesses they bet against. These players exploit the system, driving down stock prices to line their pockets, sometimes at the expense of legitimate companies.

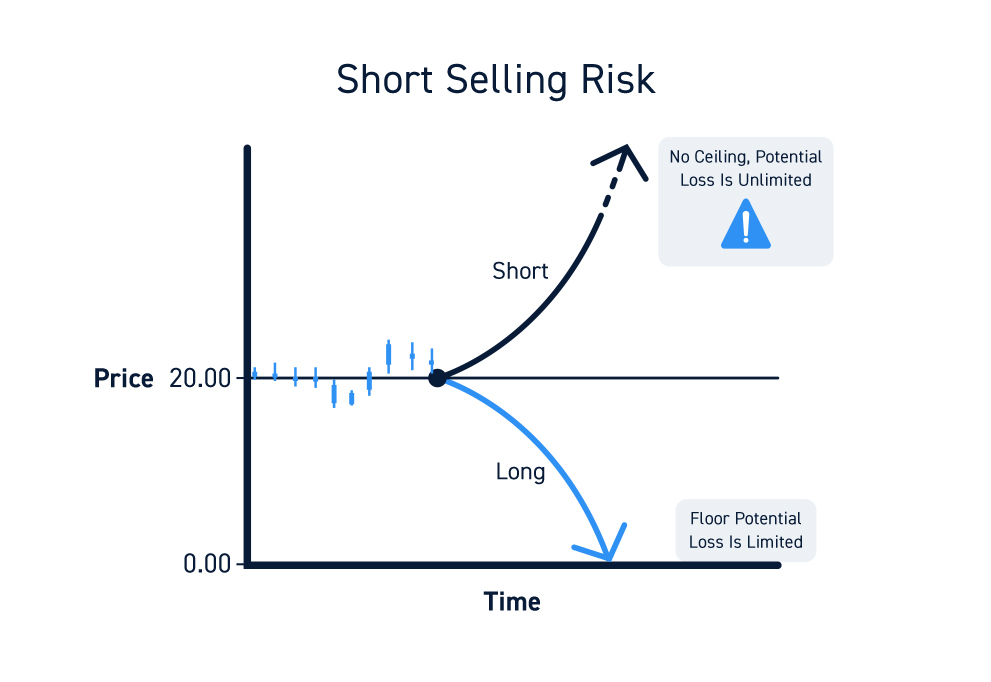

However, there’s one inescapable truth about short-selling: while the potential upside is capped at 100%, the downside risk is limitless.

This imbalance means you need to be absolutely certain in your analysis because one misstep could wipe out your entire portfolio.

That’s why I was alarmed when not one, but two short-sellers, published reports on GigaCloud Technology (GCT), an e-commerce company that has been delivering remarkable results.

At first glance, GigaCloud appears to be one of the fastest-growing companies in the world, boasting to have cracked the code on large parcel logistics—a notoriously challenging sector. But as I dug deeper, I found several unsettling, unanswered questions.

Now, the question for investors is clear: Is GigaCloud Technology the next Amazon, or are we looking at a corporate mirage?

GigaCloud: Management’s Perspective

GigaCloud Technology first grabbed my attention with its standout financials. We’re talking 30.36% annual revenue growth over the past three years, a net profit margin of 13.37%, and a return on equity of 32.40%.

This led us to discuss the company in one of our recent podcasts:

Analyzing the $278 Billion Nvidia Crash, the Canadian Economy, and GigaCloud Technologies | MMC #4

So, what’s GigaCloud’s secret sauce?

At the heart of its success is the GigaCloud Marketplace, a platform designed to revolutionize the large parcel market. Think furniture, appliances, gym equipment, and bulky items that typically come with high shipping and handling costs. GigaCloud bridges the gap between sellers in Asia and buyers across the U.S., Europe, and other regions, offering an efficient, cost-effective solution. The company’s footprint is strongest in the U.S., Japan, the UK, Germany, and Canada.

Their mission? To break down the barriers for third-party sellers (3P) by offering a full suite of services—marketing, data analytics, shipping, warehousing, and even last-mile delivery—at rates that undercut logistics giants like FedEx and UPS.

For buyers, this means access to a diverse range of products with faster delivery times and more competitive pricing. This is the power of the network effect—more buyers and sellers join, accelerating growth and driving GigaCloud’s rapid expansion.

But that’s not all. GigaCloud also operates a thriving first-party business (1P), selling its own products on its marketplace as well as on platforms like Amazon, Walmart, and Wayfair. In 2023, this 1P business made up a substantial 71.7% of GigaCloud’s total revenue, showing just how integrated the company is in the ecosystem.

To support this vast operation, GigaCloud has built an impressive global logistics network, consisting of 42 fulfillment centers spanning 10.5 million square feet across 13 key ports. Strategic partnerships with major shipping and trucking companies, along with white glove delivery services, ensure that GigaCloud’s supply chain is as robust as it is scalable.

The result? GigaCloud has created a seamless, end-to-end experience for both buyers and sellers—something very few companies can offer at this scale. This comprehensive approach has driven exceptional growth during its early years as a publicly traded company.

GigaCloud’s Growth Through Acquisition

One of the most interesting facets of GigaCloud’s recent expansion is its strategic acquisition moves. In 2023, the company made two notable purchases aimed at boosting its infrastructure and enhancing its competitive edge.

The first acquisition was Noble House, a $77.6 million all-cash deal completed on November 1, 2023. This acquisition significantly expanded GigaCloud’s fulfillment capabilities, adding six U.S. warehouses (totaling 2.4 million square feet) and one Canadian warehouse (0.1 million square feet) to its global network. What’s more, GigaCloud gained access to Noble House’s inventory and technology, enabling it to broaden its supplier base into India and deepen its reach in Canada. This move solidified GigaCloud’s position as a global logistics powerhouse, making it better equipped to serve diverse markets across continents.

Additionally, GigaCloud acquired Wondersign, a SaaS company specializing in e-catalog management, for $10 million in cash. Wondersign’s “Catalog Kiosk” software allows retailers to display their product offerings more effectively while improving customer engagement. With this technology in the hands of thousands of U.S. retailers, GigaCloud secured a direct connection to these storefronts, enhancing the capabilities of its marketplace. The goal? To improve the user experience, adding a layer of convenience and quality that further differentiates GigaCloud from competitors.

Though corporate acquisitions are nothing new, what makes these acquisitions particularly compelling is how seamlessly they fit into GigaCloud’s existing operations. Both deals enhance the company’s infrastructure while aligning with its long-term vision. The management’s decision to fund these acquisitions using cash reserves, rather than issuing new shares or taking on debt, is a clear signal of their commitment to shareholder value.

While it’s still too early to gauge the full impact of these acquisitions, one thing is clear: GigaCloud’s leadership is playing the long game, making smart, calculated moves to strengthen the company without putting unnecessary strain on investors. These strategic investments are positioning GigaCloud to not just keep pace with its rapid growth but to accelerate it, all while keeping shareholder interests front and center.

GigaCloud’s Operation by the Numbers

It’s easy to talk about having a superior business model, but backing it up with solid numbers is where the real story unfolds. When it comes to GigaCloud Technology, the operational growth alone is hard to ignore. This is a company firing on all cylinders, delivering performance metrics that are nothing short of extraordinary.

Take a look at GigaCloud’s key performance indicators (KPIs) from 2021:

- 3P Sellers: 382

- Active Buyers: 3,566

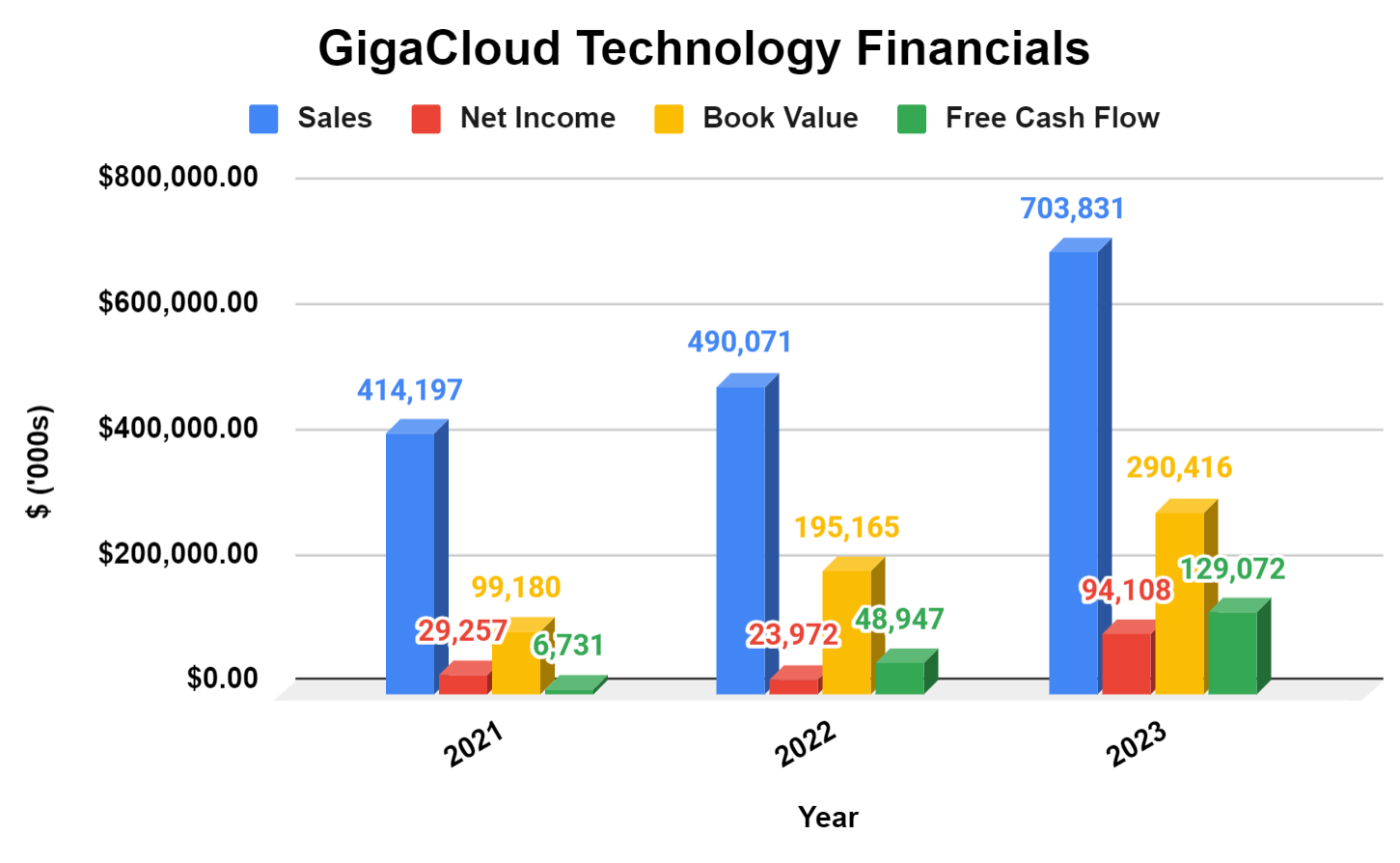

- GigaCloud Marketplace GMV: $414.2 million

- Average Spend per Buyer: $116,150

- Off-platform GMV: $127.6 million

- Total GMV: $541.8 million

- 3P Seller GMV %: 37.9%

Now, fast forward to 2023:

- 3P Sellers: 815 (+113.35%)

- Active Buyers: 5,010 (+40.49%)

- GigaCloud Marketplace GMV: $794.4 million (+91.79%)

- Average Spend per Buyer: $158,569 (+36.52%)

- Off-platform GMV: $204.6 million (+60.34%)

- Total GMV: $999.1 million (+84.40%)

- 3P Seller GMV %: 53.7% (+41.69%)

In just two years, GigaCloud has more than doubled its 3P seller base, dramatically increased its marketplace GMV, and pushed up average buyer spend. These growth rates are the kind of performance numbers most companies can only dream of.

And the momentum hasn’t stopped. As of August 2024, GigaCloud continues to outperform:

- 3P Sellers: 930 (+39.8% YoY)

- Active Buyers: 7,257 (+66.8% YoY)

- GigaCloud Marketplace GMV: $1,097.8 million (+80.7% YoY)

- Average Spend per Buyer: $151,276 (+8.3% YoY)

- 3P Seller GMV %: 52.1%

These operational results echo something Jeff Bezos pointed out in Amazon’s 2000 Annual Shareholder letter. Despite Amazon’s stock plummeting 80% that year, the company’s underlying business was thriving, steadily growing and improving.

GigaCloud finds itself in a similar situation. Even though the stock is down nearly 60% in the past six months, the company’s operational KPIs tell a completely different story.

From its meteoric rise in 3P sellers and active buyers to its impressive marketplace GMV, GigaCloud is showcasing all the signs of a company with solid fundamentals. Its financial health remains robust, management is making savvy capital allocation decisions, and its track record speaks for itself.

So, the burning question is: why are short-sellers going after a company with such remarkable growth metrics?

GigaCloud: The Short’s Perspective

On the surface, GigaCloud Technology seems like a rising star. But under the hood, there may be serious issues lurking. Recently, two prominent short-selling firms, Grizzly Research and Culper Research, released damning reports that could reshape the narrative around the company.

The allegations made in these reports paint a starkly different picture from what GigaCloud has reported to date. If the claims hold any truth, it suggests that GigaCloud’s management may be misleading not only shareholders but the entire market on a massive scale.

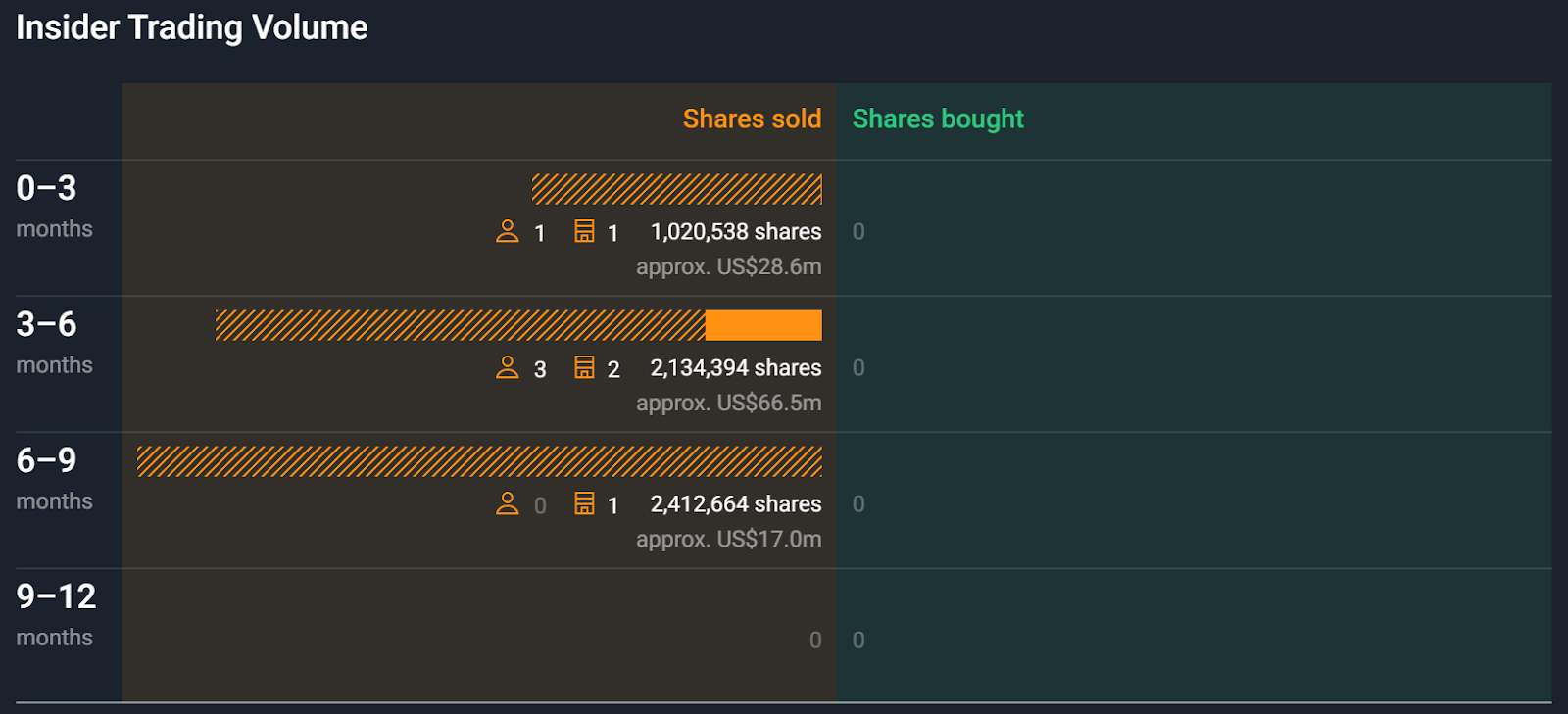

We’re talking about significant discrepancies in sales figures, profit margins, business activity, and overall financial health. Even more troubling, management has been consistently selling shares over the past year, adding fuel to investor concerns about the company’s true position.

So, what exactly did Grizzly and Culper uncover? Below are some of the key accusations from each report.

Culper Research’s Short Report

Culper Research’s Short Report was released on September 28, 2023. Here is what they claim:

- Employee and Warehouse Discrepancy: GigaCloud claims to operate 14 U.S. warehouses but has only 73 employees, implying an implausibly low number of workers per warehouse compared to industry norms, raising doubts about the company’s efficiency claims.

- Warehouse Observations: Investigators visiting GigaCloud warehouses reported minimal activity, contradicting the company’s portrayal of its operations as efficient and growing, with one warehouse showing only a single truck over a 3-hour observation period.

- Employee Testimonies on Last-Mile Business: Former employees estimate that GigaCloud’s last-mile delivery service is vastly smaller than reported, completing far fewer deliveries and generating a fraction of the revenue the company claims.

- Artificial Intelligence Exaggerations: GigaCloud claims AI is optimizing its supply chain, but there is no evidence of AI development expenses or staff, suggesting the company’s statements may be empty marketing claims to mislead investors.

- Undisclosed Related Parties: The company appears to be connected to undisclosed entities involved in furniture trading, potentially raising issues of related-party transactions or more serious financial improprieties.

- “China Hustle” Red Flags: GigaCloud shows signs of potentially fraudulent practices, with a China-based auditor, a large portion of its cash held offshore, and suspiciously low-interest income, raising concerns about the transparency of its financial operations.

Grizzly Research’s Short Report

Not long after, Grizzly Research released its Short Report on May 22, 2024. Here is what the firm alleges:

- Stock Surge on Misunderstood Platform: GigaCloud’s stock had surged due to excitement around its meteoric rise, but web traffic data suggests the platform’s growth is exaggerated, likely involving transactions with undisclosed shell companies.

- Fraudulent Practices in 1P Revenue: Former employees revealed that many of GigaCloud’s supposed 1P buyers are shell companies lacking balance sheets and inventory, designed to create the illusion of growth and marketplace activity.

- Fulfillment Costs Hidden as Revenue: GigaCloud likely disguises fulfillment costs as 3P revenue, overstating its financial performance by booking the entire revenue for services provided by third-party logistics companies like UPS and FedEx.

- Shell Companies in Imports: Over half of GigaCloud’s U.S. imports go to shell entities, many of which lack a physical presence or valid corporate records, raising concerns about fraudulent business practices.

- Suspicious Acquisitions and Related Parties: GigaCloud’s acquisition of struggling companies like Noble House and involvement with undisclosed related parties suggest the company is using questionable tactics to prop up its growth narrative.

- Auditor and Executive Stock Sales: GigaCloud’s auditor has a limited track record, and its executives, including the CEO, have sold over $85 million in stock, raising further red flags about the company’s integrity.

Management’s Response to the Allegations

When a company faces a short report, it doesn’t necessarily need to respond. If the allegations lack merit or the company’s fundamentals speak for themselves, there’s no need to engage with firms like Grizzly Research or Culper Research. In time, the truth will emerge, and any baseless claims will fade into insignificance.

However, when a company does choose to respond, it must do so with full transparency and irrefutable evidence to address each point. In GigaCloud Technology’s case, the decision to confront the short sellers head-on signals confidence—but did the company do enough to clear the air?

Let’s start with GigaCloud’s response to Culper Research’s report, where the company refuted four key claims:

- Warehouse Operations: Culper’s claim about GigaCloud’s U.S. warehouses being understaffed is misleading, as the company uses third-party staffing agencies and contractors, a fact disclosed in its SEC filings.

- Transportation Network: The report misrepresents GigaCloud’s delivery services, failing to understand that the company uses its own trucks mainly for white glove services and third-party providers for other deliveries, which is disclosed in its SEC filings.

- Cash Balances: The company’s cash balances, questioned by the short seller, have been audited and verified by KPMG, with an unqualified opinion confirming $181.5 million as of June 30, 2023.

- Related Party Transactions: GigaCloud asserts that all related party transactions have been fully disclosed per SEC rules and accounting standards.

To reinforce its stance, GigaCloud’s board also approved an independent review, which found that Culper’s claims were unsubstantiated; though details on this review remain limited.

GigaCloud also addressed Grizzly Research’s allegations:

- Web Traffic: Grizzly’s claim about low web traffic is based on misleading third-party data focused on search engine performance rather than total website traffic, omitting estimates showing GigaCloud had around 130,000 visits and 11,000 unique visitors in April 2024.

- B2B Model: GigaCloud operates a B2B marketplace with resellers, not direct consumers, meaning its business model involves selling in volume to a smaller customer base, and the traffic reported aligns with its disclosed 5,010 active buyers in 2023.

- Related Party Transactions: The allegations of undisclosed related party transactions are false, as GigaCloud has disclosed all required relationships and the legitimacy of sales is supported by documented deliveries and logistics expenses.

- Short-Seller Bias: The report contains unsupported claims and personal attacks, with the short seller disclaimer admitting that their views should not be considered factual and are designed to profit if the company’s stock declines.

While GigaCloud did a solid job of addressing inaccuracies and defending its business practices, the company seemed to sidestep some of the most critical concerns. Grizzly and Culper raised deeper issues around the use of shell companies, fulfillment cost discrepancies, and inactive warehouses—claims that go right to the heart of GigaCloud’s business fundamentals.

Instead of confronting these red flags head-on, GigaCloud’s management chose to focus on relatively minor details like employee numbers, delivery service types, and web traffic. These are valid points, but they don’t get to the crux of the short reports’ most damaging accusations.

For an investor seeking clarity, the lack of a direct response to these major issues raises questions. Why gloss over concerns about shell companies or unaccounted fulfillment costs? Why not provide more transparency around warehouse operations beyond staffing numbers?

The ambiguity in GigaCloud’s responses felt like a missed opportunity for the company to put these concerns to rest. For a business with such impressive growth metrics, the failure to fully address critical allegations left me with doubts about its long-term prospects.

The Verdict: Passing Up on GigaCloud Technology

I always take short reports with a grain of salt. These firms profit when a stock’s price plummets, so it’s no surprise they focus on highlighting the negative. But in the case of GigaCloud Technology, something is unsettling about the level of detail and investigation conducted by both Grizzly Research and Culper Research.

What makes these reports compelling isn’t just the claims, but the due diligence behind them. Both firms dug deep—speaking with current and former employees, visiting GigaCloud’s warehouses, and pulling public records on supposed customers. It’s hard to believe that either Grizzly or Culper would fabricate this much information, knowing full well the legal risks they’d face from defamation or other consequences.

Even more concerning is GigaCloud’s response. Management failed to effectively address the most serious allegations, leaving too many questions unanswered. While GigaCloud refuted certain points, like staffing issues and web traffic, it dodged some of the bigger concerns—such as shell company allegations, fulfillment discrepancies, and warehouse inactivity.

That’s not to say I’m taking everything in these short reports at face value. But with so many red flags and too few solid answers, I’ve decided to step away from GigaCloud for now. Until the company can definitively prove that the major concerns raised by Grizzly and Culper are baseless, the risk of this investment turning into a costly mistake feels too high.

I genuinely hope the accusations are unfounded. But until GigaCloud provides real transparency, it’s too early to say for certain. I highly encourage you to dig into the company’s financials, read the annual reports, and review the short reports from Grizzly and Culper. You might come to a different conclusion than I did. But for now, I’m comfortable passing on this one.

Disclaimer/Disclosure:

We are not brokers, investment, or financial advisers, and you should not rely on the information herein as investment advice. If you are seeking personalized investment advice, please contact a qualified and registered broker, investment adviser, or financial adviser. You should not make any investment decisions based on our communications. Our stock profiles are intended to highlight certain companies for YOUR further investigation; they are NOT recommendations. The securities issued by the companies we profile should be considered high risk and, if you do invest, you may lose your entire investment. Please do your research before investing, including reading the companies’ public filings, press releases, and risk disclosures. Information contained in this profile was provided by the company, and extracted from public filings, company websites, and other publicly available sources. We believe the sources and information are accurate and reliable but we cannot guarantee it. The commentary and opinions in this article are our own, so please do your research.

Copyright © 2024 Micro Math Capital, All rights reserved.