“I don’t look to jump over 7-foot bars: I look around for 1-foot bars that I can step over.” — Warren Buffett

Investing in small-cap companies offers a unique advantage: simplicity. These businesses often operate with lean, focused models that are far easier to understand than the sprawling empires of large-cap giants. Pair that simplicity with a brilliant management team, and you’ve got a recipe for outsized success.

Yet, paradoxically, many investors flock to industry titans, mistaking familiarity for simplicity. Their size and presence offer a comforting sense of security. But beneath the surface lies a labyrinth of complexity: sprawling business units, intricate supply chains, countless subsidiaries, and an army of employees. For the average investor, understanding the fundamentals of these behemoths can feel like decoding an encrypted message.

This is true in an industry like oil and gas where businesses like ExxonMobil, Chevron, and Shell dominate the headlines. But, if you search under the hood of a company like Exxon, you’ll find a corporation managing over $461.9 billion in assets and $185.5 billion in liabilities. Miss a key detail, and it could cost you.

Now, imagine taking a different path—a simpler, more transparent one. Instead of wrestling with the complexities of mega-cap giants, focus on small-cap opportunities where the story is clear, the fundamentals easy to grasp, and the growth potential untapped.

Take Tenaz Energy as a case in point. This small-cap oil and gas company embodies Buffett’s philosophy of stepping over 1-foot bars. Tenaz offers the best of both worlds: robust financial performance and a straightforward business model. With fewer moving parts and easily trackable developments, it allows investors to stay close to the action and understand exactly how value is created.

Tenaz also meets the cornerstone criteria of smart investing:

- Proven management with a track record of success.

- Strong financials that demonstrate stability and growth potential.

- Attractive valuation—purchasing shares at a discount to intrinsic value.

By diving into Tenaz Energy’s story, you’ll gain not only a deeper understanding of this specific opportunity but also a replicable blueprint for successful small-cap investing.

If you’re ready to embrace simplicity and seek out 1-foot bars in your investment journey, this could be your moment. The next great opportunity doesn’t have to be hidden within a labyrinth of complexity—it could be right in front of you, clear and accessible.

Tenaz Energy’s Journey So Far…

Over the past year, Tenaz Energy’s stock price has skyrocketed by 235%, adding roughly $227 million to its market valuation. This is no accident; it is the direct result of prudent capital allocation and a razor-sharp strategy.

At its core, Tenaz Energy operates with a refreshingly simple yet powerful model: acquire and optimize free cash flow-producing oil and gas assets. This focused approach traces back to October 2021, when President and CEO Anthony Marino, alongside his seasoned team, took the reins by acquiring Altura Energy and rebranding it as Tenaz Energy.

The Leduc-Woodbend Project: A Sound Foundation

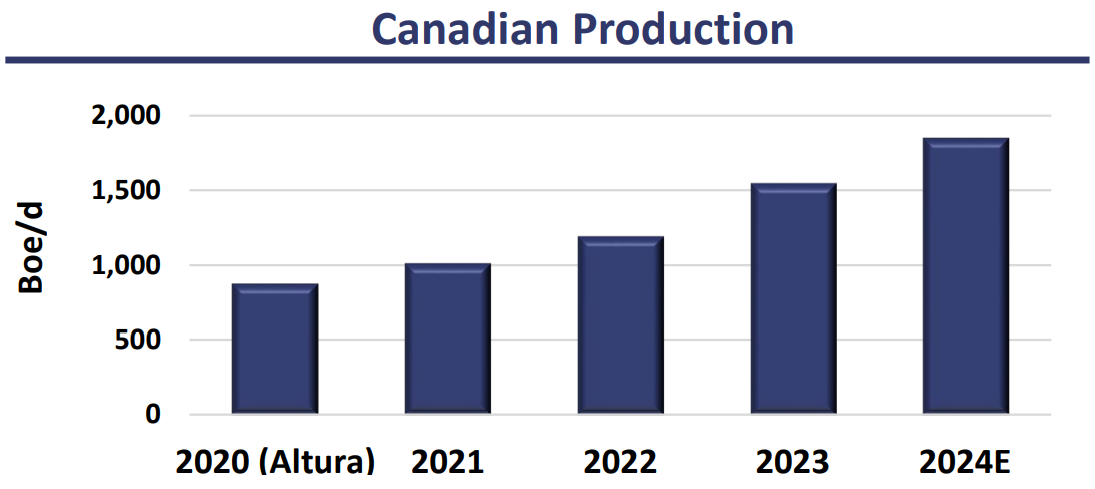

Central to this transformation was the Leduc-Woodbend Project, located in Alberta’s prolific Mannville formation. Inheriting a production base of 1,100 barrels of oil equivalent per day (boe/d), with 60% of that in oil and natural gas liquids (NGLs), Marino recognized the immense potential.

He highlighted its advantages: robust drilling economics, a contiguous land base, substantial infrastructure access, and minimal abandonment obligations.

This project became the cornerstone of Tenaz Energy’s resurgence. Fast forward to Q3 2024, and Leduc-Woodbend’s performance speaks volumes, with production averaging 1,537 boe/d and 2P reserves totaling approximately 13 million boe by the end of 2023.

Global Ambitions, Strategic Expansion

But Tenaz’s vision extended far beyond Alberta. In his first quarterly address as CEO, Marino unveiled the company’s bold expansion strategy. His goal? To broaden Tenaz’s geographic reach, seeking high-quality assets in Europe, the Middle East and North Africa (MENA), and South America.

Marino’s rationale was clear:

“We prefer to have a wide set of assets to choose from as we search for the highest returns for shareholders. Once we have made cornerstone acquisitions in one or two of these regions, we will pursue follow-on acquisitions and asset development to create meaningful scale […] The lowest risk assets for returns to shareholders will be from fields that are already producing, and this will be the primary focus of our acquisition efforts.”

This disciplined approach to global asset selection has laid the groundwork for Tenaz to scale quickly and efficiently, without compromising shareholder value.

From the get-go, Marino provided a blueprint for Tenaz Energy’s future. And so far, they have delivered.

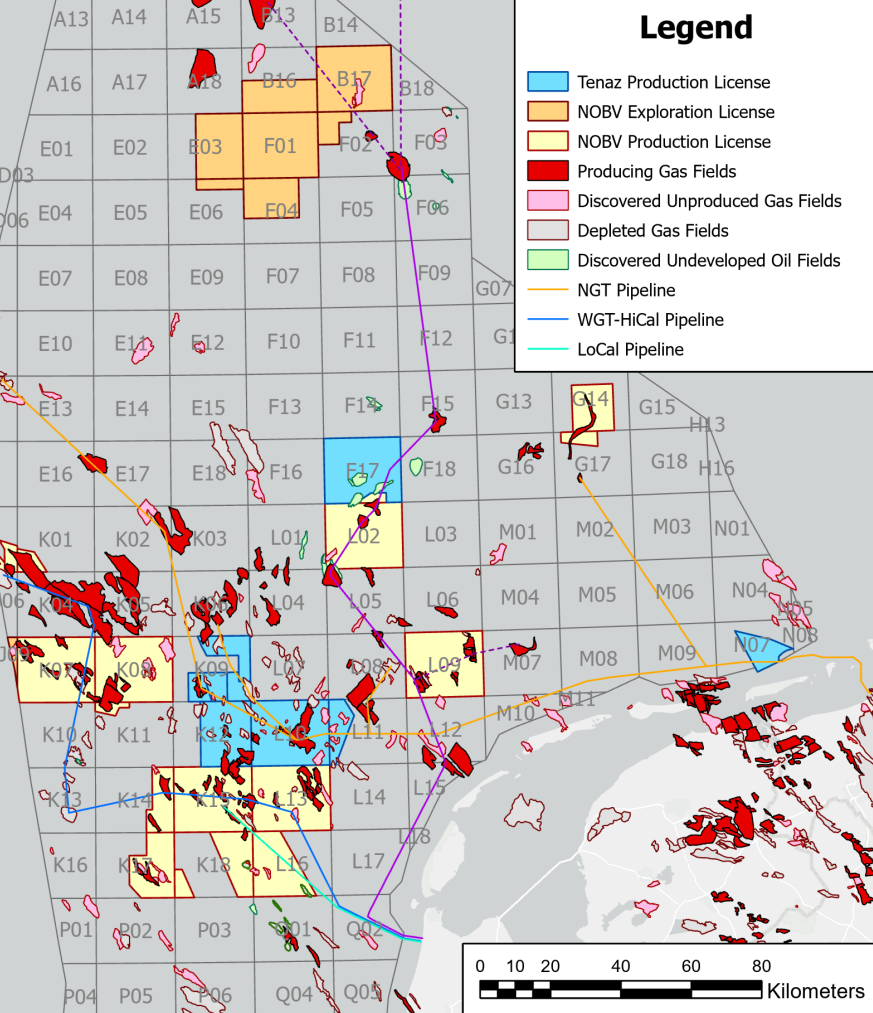

Tenaz Energy’s Entrance into the Dutch North Sea

In December 2022, Tenaz Energy executed a strategic acquisition that expanded its footprint into the Dutch North Sea, positioning itself for both near-term cash flow and long-term growth. This wasn’t just an ordinary acquisition—it was management’s first demonstration of prudent capital deployment and innovative value creation.

Tenaz acquired 100% of a private firm with both upstream and midstream assets in the Netherlands. The price? Not the typical hefty upfront cash payment. Instead, Tenaz agreed to assume the future decommissioning liabilities of the acquired assets.

At first glance, these liabilities might seem daunting—valued at $58.9 million (€40.9 million) as of January 31, 2022. But here’s where the ingenuity of this deal comes into play. By early 2023, the liabilities were projected to plummet to just $16.9 million (€11.8 million), thanks to a combination of completed decommissioning activities and surging European natural gas prices. This rapid reduction provided an immediate boost to Tenaz’s financial flexibility.

To fund the acquisition and meet its initial obligations, Tenaz utilized a $25 million credit facility, supplemented by cash on hand. However, this was no long-term burden. By leveraging the projected reduction in decommissioning security requirements, Tenaz fully repaid the credit facility in Q1 2023—within months of closing the deal.

This approach not only avoided standard acquisition costs, but it also provided non-dilutive financing, essentially debt-free growth, and assets adding immediate value. By all accounts, it was a masterclass in structuring business acquisitions.

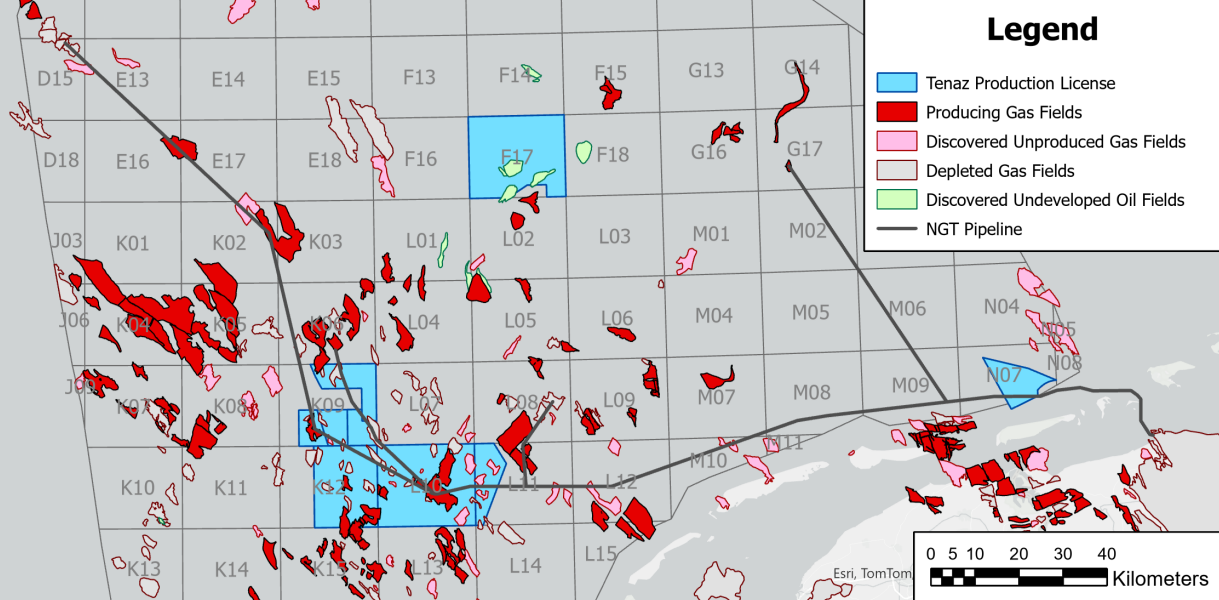

But the purchase brought more than just potential—it delivered results. Tenaz gained 5 mmcf/d of natural gas production across nine offshore licenses operated by Neptune Energy, with an average working interest of 8.4%. These assets contributed approximately 809 mboe of proved developed reserves and 1,214 mboe of total proved plus probable reserves.

But the real prize? An 11.34% stake in Noordgastransport B.V. (NGT), one of the largest gas-gathering and processing networks in the Dutch North Sea. Spanning nearly 500 km of pipelines, NGT boasts a stunning 99.8% uptime record over three decades. Tariff revenue from NGT not only provides a steady income stream but also offsets some of Tenaz’s operating costs, enhancing cash flow stability.

For 2023, Tenaz projected 750 boe/d from the acquired assets—boosting production by 50% compared to its initial guidance. The assets were expected to generate approximately $23 million (€16 million) in funds flow from operations (FFO), equating to $0.82 per share without diluting shareholder equity.

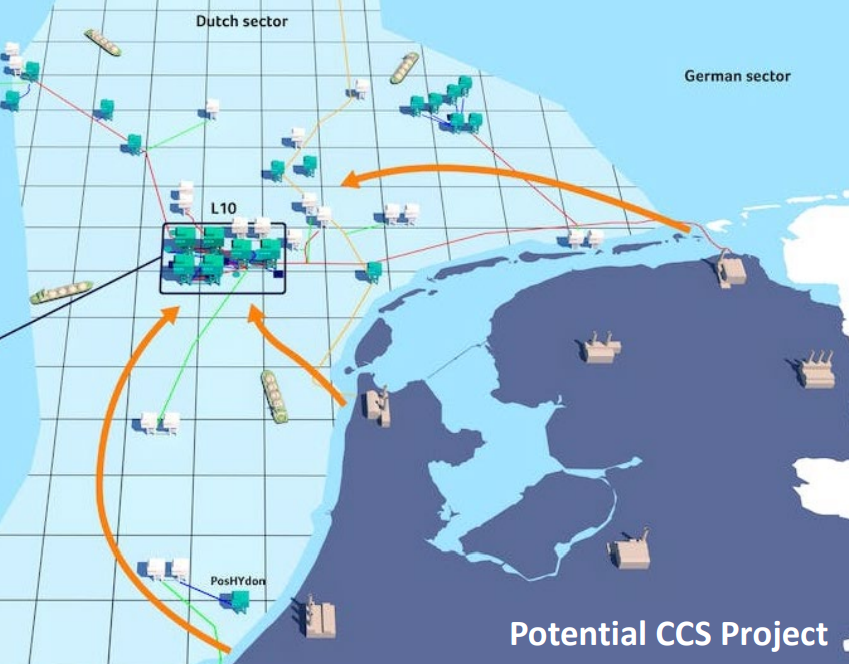

However, this acquisition wasn’t just about hydrocarbons. Tenaz also gained a stake in the L10 Carbon Capture and Storage (CCS) Project, an ambitious initiative to reuse hydrocarbon infrastructure to capture 5 to 8 megatons of CO₂ annually for up to 30 years. Once complete, it could make Tenaz carbon-neutral at production levels exceeding 50,000 boe/d, significantly extending the life of key assets and deferring decommissioning costs.

In all, it underscored Tenaz Energy’s ability to seize opportunities that deliver immediate cash flow, enhance shareholder value, and position the company for sustainable growth. It’s a testament to how thoughtful capital allocation, an innovative strategy, and operational excellence can unlock extraordinary value in a complex industry.

But it was only getting started…

Tenaz Energy Buys XTO Netherlands

Following a similar strategy, Tenaz bought XTO Netherlands from ExxonMobil in June 2023. Like the first deal, Tenaz would assume future decommissioning liabilities rather than shelling out massive upfront capital.

The acquired assets were valued at approximately $29.2 million (€20.1 million), but Tenaz had a clever financial twist. It utilized $15.3 million (€10.5 million) of cash held within XTO Netherlands to offset decommissioning obligations, effectively lowering the net cost and bolstering financial flexibility.

In return, it significantly expanded Tenaz’s working interest in several of the key offshore license blocks, enhancing its production capacity to:

- L10/L11a: From 11.35% to 21.43%

- K9a and K9b: From 8.44% to 15.94%

- K9c: From 6.49% to 12.26%

- K12: From 5.67% to 10.71%

- N7b: From 9.45% to 17.86%

While interests in the undeveloped licenses, such as F10, F11a, F17, and F18 remained unchanged, Tenaz’s strategic expansion in producing fields laid the groundwork for sustained growth.

On top of that, the company increased its ownership in Noordgastransport B.V. (NGT), rising from 11.34% to 21.4%. This move made Tenaz the second-largest shareholder in NGT.

It also provided Tenaz with sizable dividends, increasing its annual income by a meaningful amount. For example, in 2022, NGT shareholders were paid $27.0 million (€18.4 million) in dividends–the pipeline company has consistently paid dividends to its shareholders for more than 20 consecutive years.

In total, the XTO Netherlands acquisition added 664 mboe of 2P reserves (99% natural gas), with the assets projected to have a productive life of 13 years.

For 2023 alone, these assets were expected to produce 450–500 boe/d, representing a 20% increase in production per share compared to the midpoint of Tenaz’s guidance, at the time. What’s more, they were forecasted to generate $7.4 million (€5.1 million) in FFO for the year—though the final amount depended on the deal’s closing timeline.

Once again, the company showed that it could find diamonds in the rough while providing immediate value to shareholders. However, it was only until its next deal that things really heated up.

Tenaz Energy Buys NAM Offshore BV

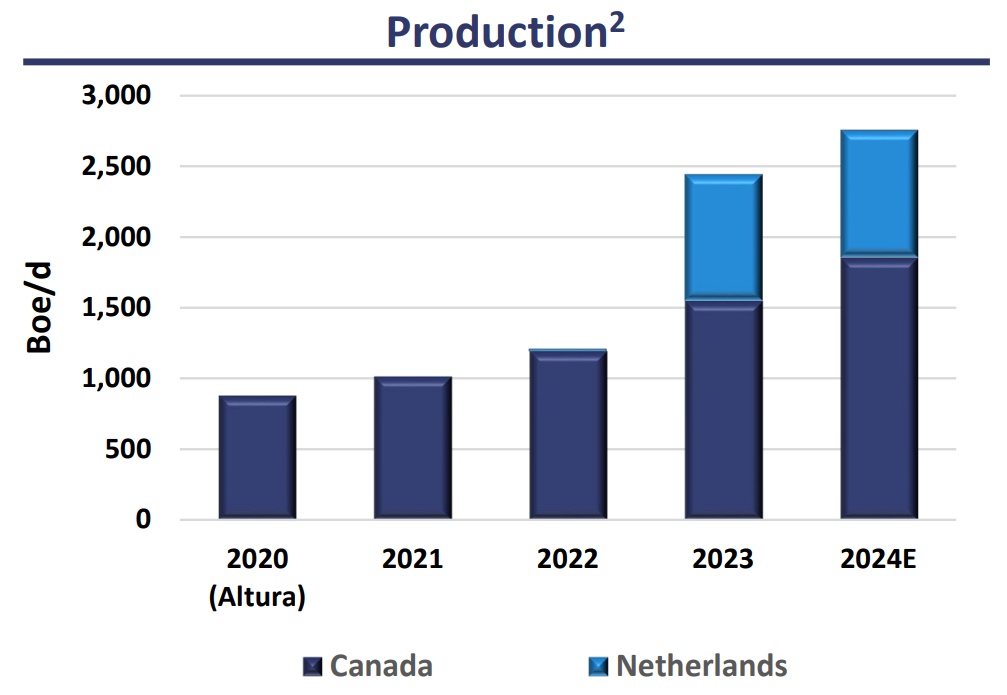

By mid-2024, Tenaz Energy was already riding high, with robust assets like the Leduc-Woodbend Project and a growing portfolio in the Dutch North Sea. The company was generating 2,535 boe/d and $3.4 million in funds from operations (FFO) in Q3 2024, with full-year guidance targeting 2,700–2,900 boe/d.

But then came the announcement that shook the market: Tenaz was acquiring NAM Offshore BV (NOBV) from Shell and ExxonMobil—a deal that would take the company’s growth to an entirely new level.

The structure of the NAM Offshore BV acquisition wasn’t just bold—it was brilliant. Unlike previous deals, this one came with a hefty price tag: $246 million (€165 million) in base consideration, plus contingent payments. To secure the transaction, Tenaz paid a $34 million (€23 million) cash deposit and secured a $90 million credit facility from National Bank of Canada.

The masterstroke? Tenaz would begin realizing free cash flow (FCF) from NAM Offshore BV as of January 2024—a full year before the deal’s anticipated close in mid-2025. NAM is projected to generate $134 million (€90 million) in free cash flow this year, with additional cash flow secured through physical fixed-price and collar hedges extending into 2026.

Effectively, Tenaz set up a situation where NAM’s assets would pay for their acquisition, a clever “infinite money glitch”.

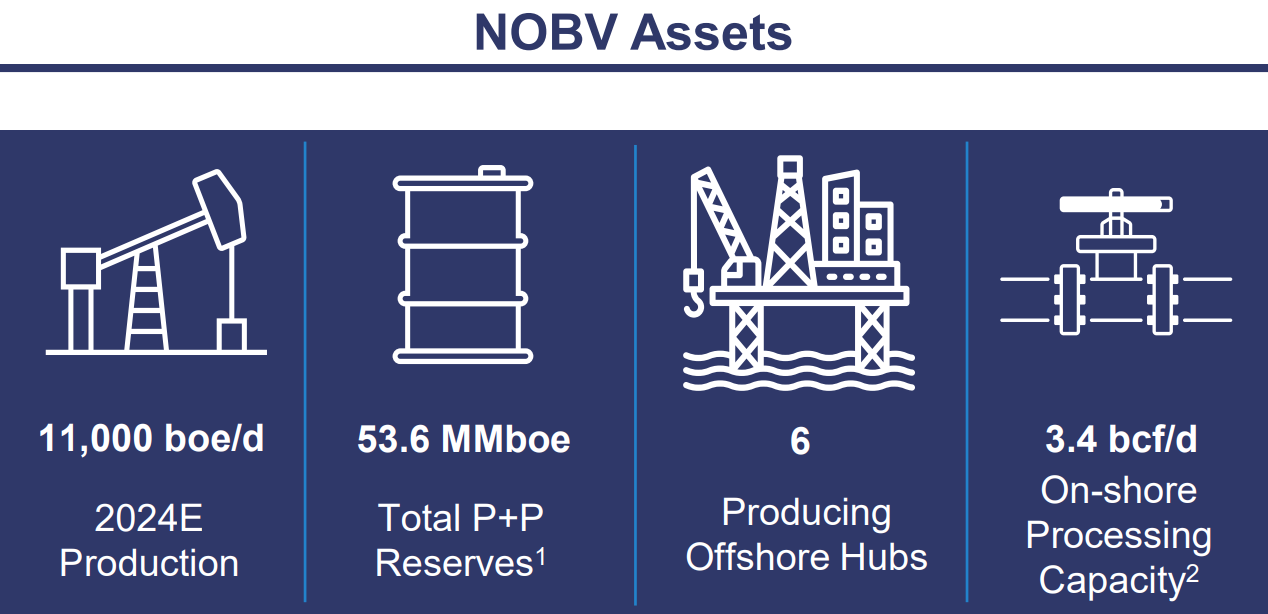

But this acquisition wasn’t just about securing cash flow—it fundamentally transformed Tenaz’s size and value:

- Production: A 3.9x increase, adding approximately 11,000 boe/d (99% natural gas).

- Reserves: A 3.7x increase in 2P reserves, totaling 53.6 million boe.

- Reserve Value: A 6.2x increase in the 2P reserve valuation.

- Became the 2nd Largest Operator in the Dutch North Sea

While this was a major win for Tenaz, there are a few contingent agreements that you should be aware of:

- Earn-Out Payments: Between 2025 and 2027, NAM will receive a percentage of NOBV’s FCF:

- 50% of 2025 and 2026 FCF

- 25% of 2027 FCF, capped at €120 million in total.

- Volume-Based Royalties: If a new field discovery on NOBV licenses surpasses certain thresholds, NAM will receive royalty payments.

- Gas Price Contingent Payments: Between 2028 and 2031, if the average realized TTF gas price exceeds €50/MWh, NAM will receive a share of the incremental after-tax cash flow.

These contingencies ensure a win-win scenario. NAM remains incentivized to support the long-term success of the assets while Tenaz gained massive immediate productivity gains.

To say the least, the NOBV acquisition was the icing on the cake. Tenaz Energy proved that it could consistently find accretive projects that would enhance the business’s value without diluting shareholders. Not only did this highlight management’s business prowess but it also demonstrated their ability create unique deal structures that optimize long-term performance.

This has set a high standard for Anthony Marino and the team, but I am confident that they will continue to deliver.

What’s Next for Tenaz Energy?

While no formal announcements have been made, the signs suggest that Tenaz Energy might be positioning itself for another transformative acquisition. And if history is any indication, this could be yet another carefully crafted, value-driven play.

In a move that caught the market’s attention, Tenaz recently secured $140 million in Senior Unsecured Notes from institutional investors.

Interestingly, part of this funding will replace the $90 million delayed-draw term loan previously arranged with National Bank of Canada to finance the NAM Offshore BV acquisition. But here’s the kicker: the fresh debt far exceeds the amount required to cover NAM. This leaves tens of millions in capital unaccounted for—capital that’s likely earmarked for something bigger.

Tenaz’s past deals have been masterclasses in financial prudence and shareholder value creation. With an annual interest rate of 12% on the notes and principal due in 2029, it’s clear that management isn’t planning to let this capital sit idle. The high cost of debt signals urgency: Tenaz likely intends to deploy these funds quickly, pursuing high-return assets that can more than offset borrowing costs.

Given the company’s extensive footprint in the Dutch North Sea and its ambitions to explore Europe, MENA, and South America, there’s no shortage of opportunities. Few competitors have the expertise or appetite to operate in these regions, giving Tenaz a unique edge in securing underappreciated, cash-generating assets.

But as Tony emphasized in our recent interview, this isn’t just about expanding for the sake of it:

“It’s not about being bigger; really what we’re after is value for existing shareholders.”

Tenaz isn’t chasing scale—it’s chasing quality. The company has built its reputation on acquisitions that not only grow production but also enhance per-share metrics, delivering strong returns for investors.

With fresh capital in hand and a clear appetite for value-driven growth, the stage is set for Tenaz’s next chapter.

Final Thoughts

Tenaz Energy’s leadership has proven, time and again, that they are masters at uncovering high-value opportunities in the oil and gas sector. Their track record speaks volumes: every acquisition has been meticulously crafted to deliver immediate and lasting returns, all while safeguarding shareholder interests.

They’ve achieved this with zero dilution, maintaining a sharp focus on structuring deals that not only grow production but also ensure the company’s long-term financial health.

But actions speak louder than words, and Tenaz’s leadership isn’t just talking about value creation—they’re fully committed to it. Insiders own 21% of the company on a fully diluted basis, aligning their interests directly with shareholders. Their financial success hinges on Tenaz’s performance, ensuring they’re just as invested in the company’s future as every shareholder.

Simply put: If Tenaz wins, we all win.

The good news is that, to date, Tenaz has consistently delivered, with a track record of acquisitions that are both accretive and transformative. Looking ahead, the company’s five-year production target of 50,000 to 100,000 boe/d highlights its bold ambition. And with a market cap of just $366 million, there’s a significant runway for growth.

If you are seeking companies with a simple, yet proven strategy, Tenaz Energy should be on the top of your list. The Calgary-based business is built for success.

Disclosure:

We are not brokers, investment, or financial advisers, and you should not rely on the information herein as investment advice. If you are seeking personalized investment advice, please contact a qualified and registered broker, investment adviser, or financial adviser. You should not make any investment decisions based on our communications. Our stock profiles are intended to highlight certain companies for YOUR further investigation; they are NOT recommendations. The securities issued by the companies we profile should be considered high risk and, if you do invest, you may lose your entire investment. One or more Micro Math Capital employees own shares in Tenaz Energy. Please do your research before investing, including reading the companies’ public filings, press releases, and risk disclosures. Information contained in this profile was provided by the company, and extracted from public filings, company websites, and other publicly available sources. We believe the sources and information are accurate and reliable but we cannot guarantee it. The commentary and opinions in this article are our own, so please do your research.

Copyright © 2024 Micro Math Capital, All rights reserved.