The maritime shipping industry is a pillar of the global economy, keeping the wheels of trade turning. As Warren Buffett once said about rail systems, “Our country’s future prosperity depends on it having an efficient and well-maintained” infrastructure. This rings just as true for chartered shipping.

Without a reliable and sufficient fleet of chartered vessels, global trade would be at risk, and economic pressures would drive up shipping rates to unsustainable levels. This is precisely why companies like Euroseas (ESEA) are indispensable to the economy. Euroseas plays a vital role in transporting millions of goods safely and efficiently across the globe, maintaining the delicate balance of supply chains and economic stability.

Yet, despite its importance and a remarkable stock performance—up 66% in the past year and an impressive 872% over the last five—Euroseas remains undervalued, with a P/E ratio of just 2.43. This discrepancy reflects the market’s lack of recognition for a company with both an impressive track record and significant upside.

Euroseas’ story goes back over 140 years, rooted in the legacy of a four-generation family-owned business. The company’s deep expertise and strategic approach reflect the resilience and precision only such experience can bring. Operating with a streamlined and highly effective business model, Euroseas has paired its heritage with modern operational excellence, making it one of the most fundamentally sound and enduring companies in the world.

In an industry currently marked by volatility, Euroseas stands out as a bastion of stability and growth. Its time-tested approach, paired with sound financials and a clear vision for the future, makes it a compelling opportunity. No matter what the market throws its way, Euroseas is built to last—positioned for not just the next quarter, but possibly another 140 years. Here’s why.

The Rich History of Euroseas (ESEA)

Euroseas holds one of the most storied legacies in the shipping industry—a legacy that stretches back more than 140 years to an era when the seas were ruled by sail. Founded in 1873 by Nikolaos F. Pittas, the company’s beginnings were humble yet deeply ambitious. Nikolaos owned and operated a 700-ton wooden sailing vessel, the Ypapanti, navigating the Mediterranean and Black Seas with a crew made up of his younger brothers and other relatives.

Business was thriving, and by 1876, Nikolaos was able to expand his fleet. He acquired the Sotiras, a 780-ton vessel, and in 1878 commissioned the Chios, a 1,000-ton barque. More ships would follow as Nikolaos diversified his operations, even taking on the role of managing director of “The Two Sisters,” a ship insurance company that covered a vast number of Chian sailing vessels until steam-powered ships transformed the industry.

At the dawn of the 20th century, Nikolaos renamed the company NIKOLAOS F. PITTAS AND SONS, reflecting its evolution and ambitions. In 1906, Euroseas acquired its first steam-powered vessel, the S/S Artemis, a 1,100-ton ship that would face the harsh realities of World War I, ultimately lost to a German torpedo in 1917. Despite this, the company forged ahead, adapting to new technologies and evolving with the industry.

By 2005, Euroseas reached a historic milestone, going public on the NASDAQ. Today, it remains a family-led enterprise, helmed by descendants of Nikolaos F. Pittas, who continue to steer the company forward with the same pioneering spirit that defined its beginnings.

With that said, let’s see how the business has evolved…

The Euroseas Business Today

Euroseas operates with a simple yet effective business model: building, acquiring, and running a specialized fleet of small-to-intermediate-sized container ships. Currently, Euroseas owns 23 vessels—16 feeder containerships and 7 intermediate ones—with two additional feeder ships on track for delivery in early January 2025.

With a fleet capacity of 67,073 twenty-foot equivalents (TEU) today, Euroseas will soon expand to 72,763 TEU once the new vessels arrive. This increase means the company will be able to transport an impressive 36,381 forty-foot containers across its entire fleet at once, meeting the growing global demand for efficient shipping solutions.

Central to Euroseas’ efficiency is Eurobulk Ltd., an affiliate responsible for managing the day-to-day commercial and technical operations of the fleet. This arrangement not only brings significant cost savings but also draws on Eurobulk’s extensive network and expertise in maritime logistics. Eurobulk primarily serves Euroseas and EuroDry (EDRY)—a 2018 spin-off specializing in dry-bulk cargo transportation—alongside smaller private clients. Under the leadership of President Aristides J. Pittas, Vice President Emmanuel Pittas, and Financial Manager Nikos J. Pittas, Eurobulk has developed longstanding relationships with top-tier banks, charterers, shipyards, and insurers, solidifying Euroseas’ reputation and reach in the industry.

Euroseas Target Market

Euroseas operates in the strategically selected small-to-intermediate-sized container ship market, where smaller vessels serve a unique and essential role. These vessels enable it to service shorter-distance routes and access a wide array of ports globally, many of which cannot accommodate larger ships. This creates a significant advantage, allowing the company to meet an underserved demand for agile, flexible shipping solutions in ports that mega-ships cannot reach.

Euroseas is particularly focused on the feeder market, which it believes offers the most attractive growth opportunity in the industry. Projections indicate the feeder market will expand at an annual growth rate of 3.7%, reaching $11.3 billion by 2034. By positioning itself in this high-potential segment, the business is well-poised to capture this demand growth and elevate its market standing over the coming decade.

Euroseas’ Strategy Toward Building & Acquiring Vessels

Euroseas takes a disciplined, results-focused approach to fleet expansion. When acquiring second-hand vessels or commissioning new builds, management adheres to a clear strategy: no vessel is added to the fleet unless it promises a return on equity of 15% or higher. This rigorous standard ensures that every addition contributes meaningfully to the company’s profitability.

The impending environmental regulations from the International Maritime Organization (IMO) also play a critical role in Euroseas’ acquisition decisions. Newer vessels with superior fuel efficiency will command a premium, offering cost savings and compliance advantages that older vessels may lack. However, management is not sacrificing its standard acquisition strategy for the sake of an evolving regulatory environment. The company remains adamant about acquiring and building vessels that deliver the most economic value. In other words, they will continue to operate older ships until it is no longer feasible (more on this later).

This disciplined growth strategy is reinforced by a prudent financial structure. With a low debt-to-equity ratio of 64.48%, Euroseas demonstrates financial conservatism, using leverage to fund operations without becoming over-reliant on debt. As the company continues to repay its outstanding loans, it expects improved access to favorable financing options. This enhanced borrowing capacity will enable Euroseas to expand its fleet more cost-effectively, thereby increasing its fundamental value and positioning it for long-term, sustainable growth.

Navigating the Cycles of Container Shipping

The container shipping industry is famously cyclical, with demand and supply ebbing and flowing based on economic conditions and market equilibrium. For companies in this sector, success hinges on a management team’s ability to anticipate these cycles and navigate downturns with resilience. This is where Euroseas excels, leveraging a strategic approach that balances short- and long-term charters to optimize cash flow across market fluctuations.

When Euroseas anticipates a rise in charter rates, it strategically issues shorter-term contracts, positioning itself to benefit from potential rate increases. Conversely, when the market faces pressure or rates are expected to soften, Euroseas secures longer-term contracts, locking in more favorable rates and stabilizing cash flow. This disciplined approach ensures that even during leaner periods, Euroseas covers its operating costs, including vessel management, interest expenses, and drydocking.

Take the past five years as a testament to this strategy’s success. Amid pandemic-driven supply constraints, Euroseas capitalized on record charter rates, achieving four years of consecutive record sales and profits. Yet as the market begins to stabilize, management anticipates a new phase, characterized by a growing supply of vessels and uncertain demand due to geopolitical shifts, environmental regulations, and economic pressures.

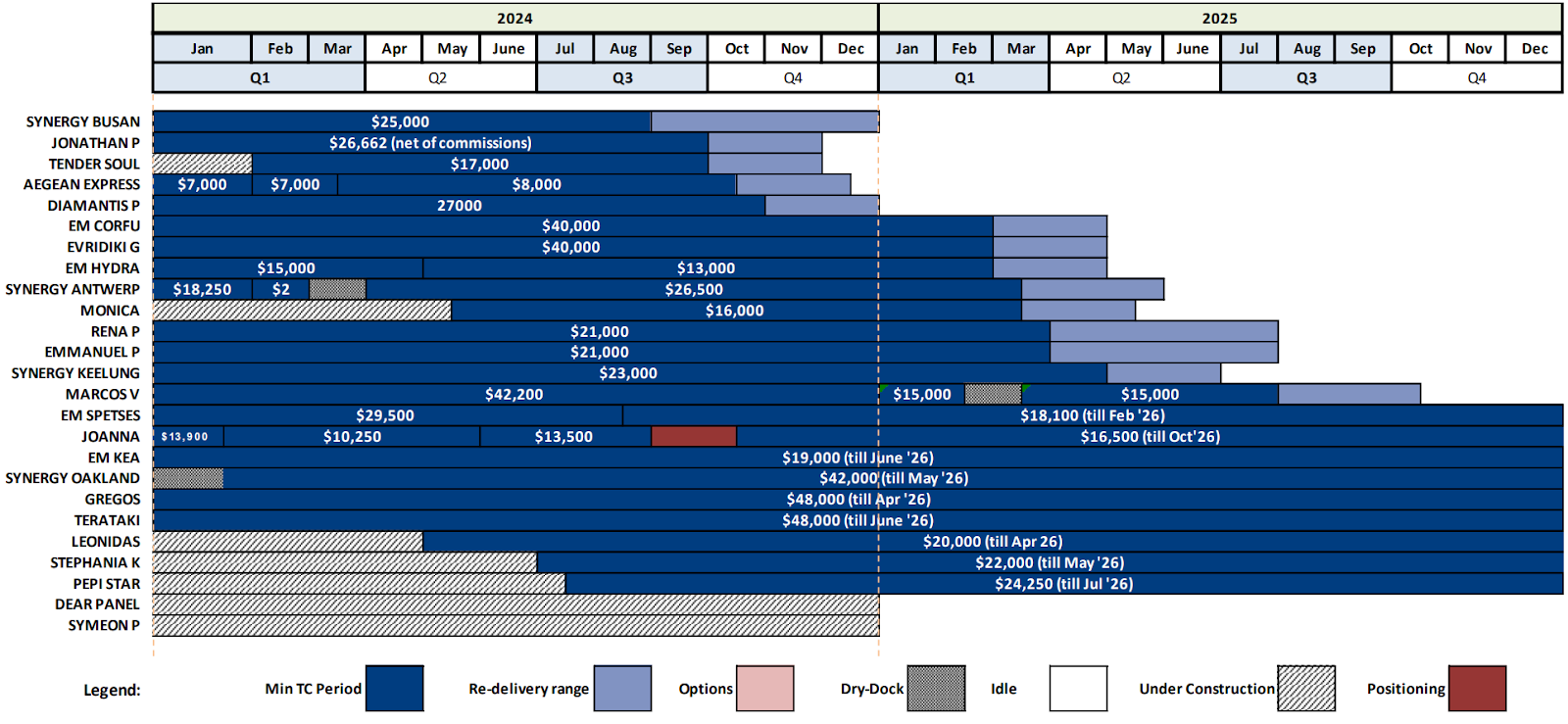

In response, Euroseas has already structured several long-term contracts to mitigate potential rate declines:

- Oct 21, 2024: Three-year contract for three 2,800-TEU fuel-efficient feeder containerships (M/V Tender Soul, M/V Dear Panel, M/V Symeon P) at $32,000/day.

- Oct 7, 2024: One-year contract for the 1,732-TEU M/V Jonathan P at $20,000/day.

- Sep 23, 2024: Three-year contract for the 4,250-TEU intermediate containership M/V Synergy Busan at $35,500/day.

- July 23, 2024: 18-month contract for the 1,740-TEU feeder containership EM Spetses at $18,100/day.

- Aug 23, 2024: Two-year contract for the 1,732-TEU feeder containership M/V Joanna at $16,500/day.

Even more vital is Euroseas’ high fleet utilization rate, which directly impacts its revenue and profitability. As of its last report, fleet coverage was at 99.9% for 2024, with 63% coverage secured for 2025 and 31% for 2026. Despite what looks like declining usage, this is standard as current charters come to an end, and new contracts emerge. By all accounts, management remains confident that it can sustain high coverage in the years ahead; a key factor to it’s longevity.

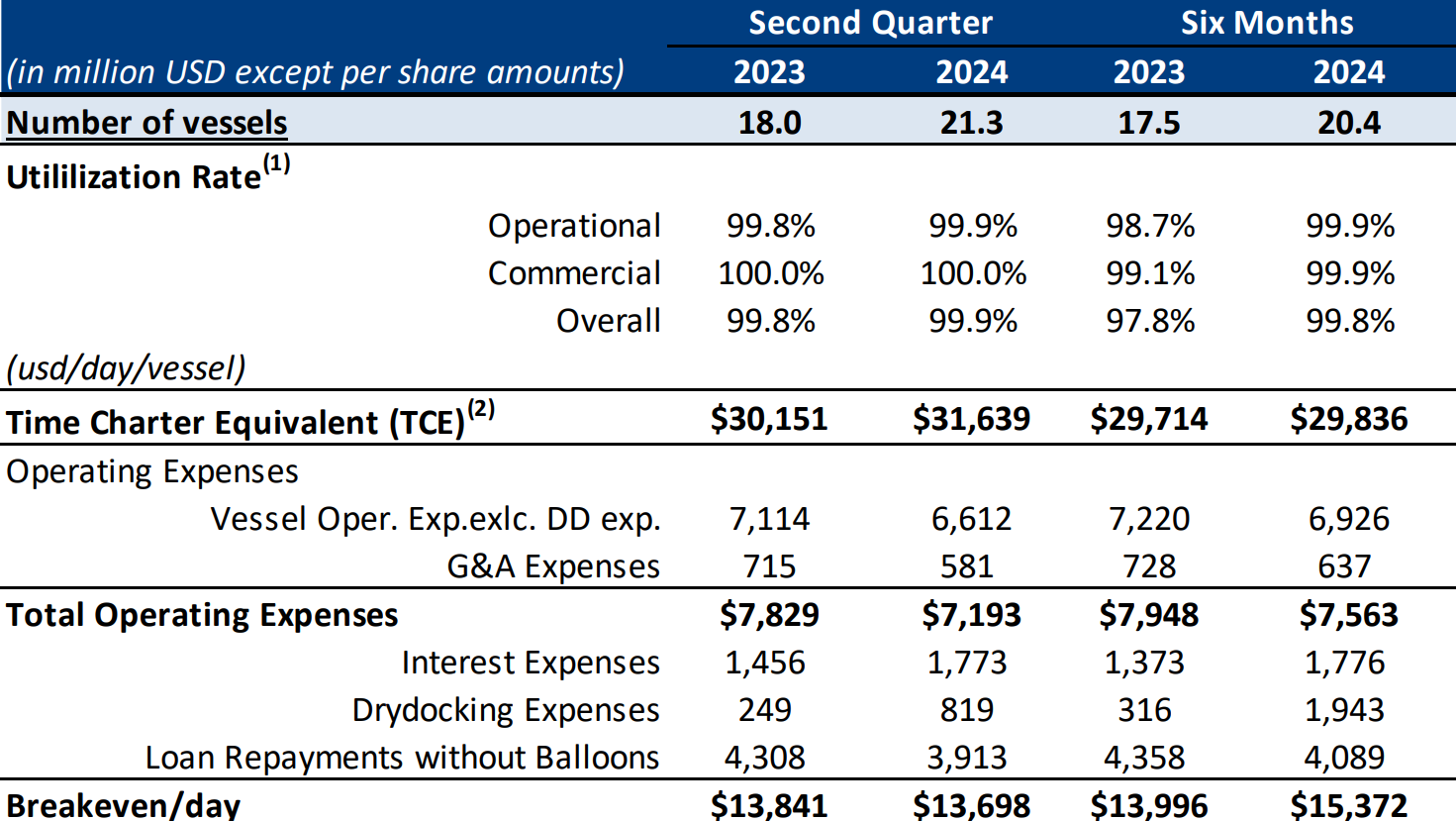

At an operational level, shipping companies use the Time Charter Equivalent (TCE) to measure the average daily net revenue per vessel. Recent figures for Euroseas show TCE in Q2 2024 above the first-half average, and importantly, well above daily operational expenses. This strong TCE, coupled with disciplined cost management, positions Euroseas to remain profitable even if charter rates were to decline by as much as 50%, underscoring the company’s efficiency and operational advantages despite the industry’s cyclicality.

Euroseas’ ability to maximize returns while maintaining robust cost control highlights its resilience and adaptability in this cyclical industry. With a strategic eye on market conditions and a conservative, well-capitalized approach, the company is poised to weather any storm and capture opportunities as they arise.

How does Euroseas Stack Up Against the Competition?

The global shipping market saw an unprecedented surge in profitability driven by pandemic-induced supply constraints, ongoing geopolitical tensions, and shifting environmental regulations. Many charter companies seized the moment, boosting revenue and profits at rapid rates. Given these industry-wide tailwinds, one might wonder if Euroseas’ recent success is simply a reflection of a rising market—or if it’s something more.

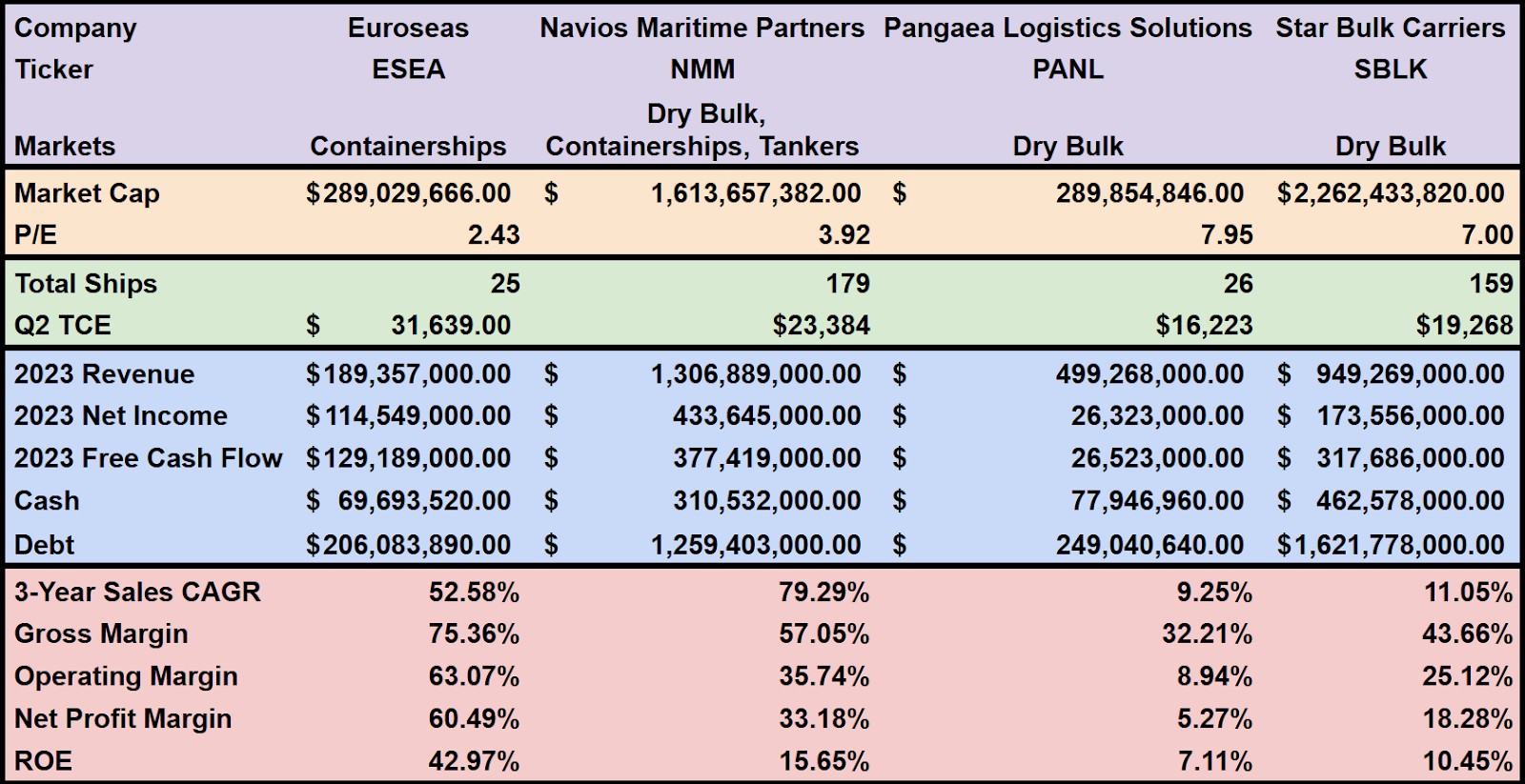

However, when you compare Euroseas’ performance with its peers, it becomes clear: Euroseas isn’t just riding the tide. With a meticulously crafted charter strategy, careful capital allocation, and a targeted focus on the container ship market (in contrast to the dry bulk and tanker sectors), Euroseas’ success is a direct result of strategic, deliberate choices made by its management.

Indeed, while the adage may say, “a rising tide lifts all boats,” Euroseas has sailed significantly ahead of the fleet. Across key metrics—gross, operating, and net profit margins, as well as return on equity for the last fiscal year (2023)—Euroseas consistently outperforms its industry counterparts. This demonstrates not only the company’s capability to generate strong returns but also its ability to control operating costs and maintain a conservative approach to debt.

The one metric where Euroseas trails is in three-year annual sales growth relative to Navios. However, if revenue growth doesn’t translate into proportional profit growth, then higher sales can be more of a liability than an asset.

To summarize, Euroseas’ performance isn’t a coincidence—it’s the outcome of a finely tuned strategy, perfected over years, that shines through every facet of the business. Management’s approach to creating value has placed Euroseas in a category of its own, setting it apart as a standout in the global shipping market.

What are Euroseas Primary Risk Factors?

While Euroseas has thrived on a combination of favorable market conditions and its own operational excellence, no investment is without risk. To fully understand the opportunity Euroseas presents, one must also consider the challenges that may impact its performance—even as management works to mitigate these factors.

Here are the top three risks every investor should consider:

1. Market Cyclicality

The global shipping market is nearing the end of a five-year expansion driven by unprecedented supply constraints. This boom has elevated charter rates and boosted profits across the industry. While current rates remain high, sustainability is uncertain, especially as new vessels are introduced to the market. Euroseas is strategically positioning itself by locking in longer-term contracts and cutting costs to endure potential downturns.

Fortunately, Euroseas has a comfortable margin between current rates and its break-even point, meaning it can remain profitable even in a significant downturn. Although the global fleet is expected to grow by 10% in 2024, ongoing supply constraints, related to an environmental regulatory shift and geopolitical conflict, may continue to support above-average rates. However, it is best to monitor these trends closely, as any sharp changes in demand could affect the company’s earnings in the coming years.

2. Age of Euroseas’ Fleet

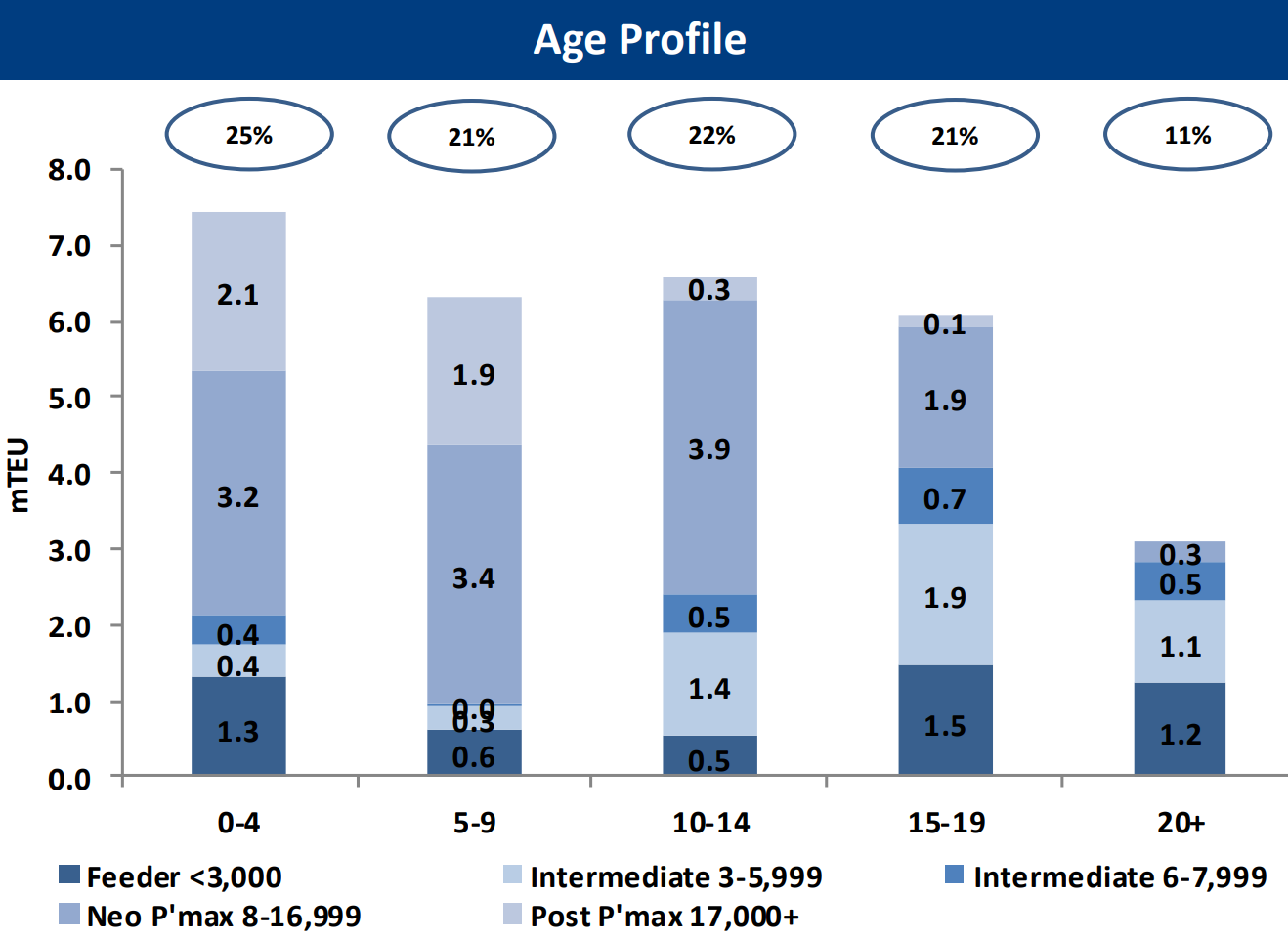

Though Euroseas is actively investing in ship acquisitions and new builds, you should be aware that several of its vessels are reaching the latter stages of their lifespan. With an average fleet age of 14 years, 16 of Euroseas’ 23 vessels (excluding its two new feeder ships to be delivered in 01/2025) were built before 2010. Typically, ships are scrapped around 25 years old, though poor market conditions or stricter regulations may accelerate this.

As Euroseas’ older ships approach the end of their useful lives, the company will face ongoing costs to acquire new vessels—a necessary expense to maintain its operational capacity. While management is committed to reinvesting in its ships and positioned financially to do so, it is only a matter of time before the company seeks out new opportunities to replenish its existing fleeting.

3. Shifting Environmental Regulatory Environment

The International Maritime Organization (IMO) has set ambitious targets for reducing greenhouse gas emissions—20% by 2030, 70% by 2040, and net zero by 2050. For Euroseas, with its older fleet, this regulatory shift brings additional costs. Operating under stricter fuel requirements will be more expensive, and sailing speed restrictions may reduce the number of charters it can perform in a given year.

That being said, slower sailing speeds are an industry-wide concern that could lead to increased rates as the number of available ships is reduced. This has the potential to offset a portion of Euroseas’ expenses, though this outcome is uncertain.

Aside from operating at slower speeds, Euroseas is investing in fuel-efficient new builds, friction-reducing paints, and AMP devices that allow docked ships to consume electricity instead of fuel oil.

But let me make it clear, management is realistic about the continued use of conventional fuels, estimating that they will remain a staple for at least 15 to 20 more years. While Euroseas will continue replacing older ships, when economically feasible, environmental regulations present an ongoing challenge that could impact its costs and operational strategies moving forward.

In the meantime, the company is expected to operate its fleet as is until the end of their useful life.

What is Euroseas Worth?

Euroseas presents a rare opportunity, standing out as significantly undervalued by virtually every measure in the industry. Currently trading at a P/E of 2.43, P/S of 1.39, and P/B of 0.90, Euroseas’ valuation metrics showcase a company with remarkable value compared to its industry peers. But one number truly drives this home: the company’s free cash flow yield, an astonishing 44.44%. For investors, this translates to an annual cash return of nearly 45% at today’s price—a rate that’s practically unheard of.

We can take it a step further by performing a Discounted Cash Flow (DCF) model. Assuming a modest 5% growth rate over the next five years, a terminal growth rate of 1.25%, and a 15% discount rate, the model derives an intrinsic value of $925.22 million or approximately $127.09 per share. Today, however, the stock trades at only $41.91 per share, giving it a market cap of just $293.94 million. This implies that at today’s price, one can purchase Euroseas with a substantial margin of safety of 68%!

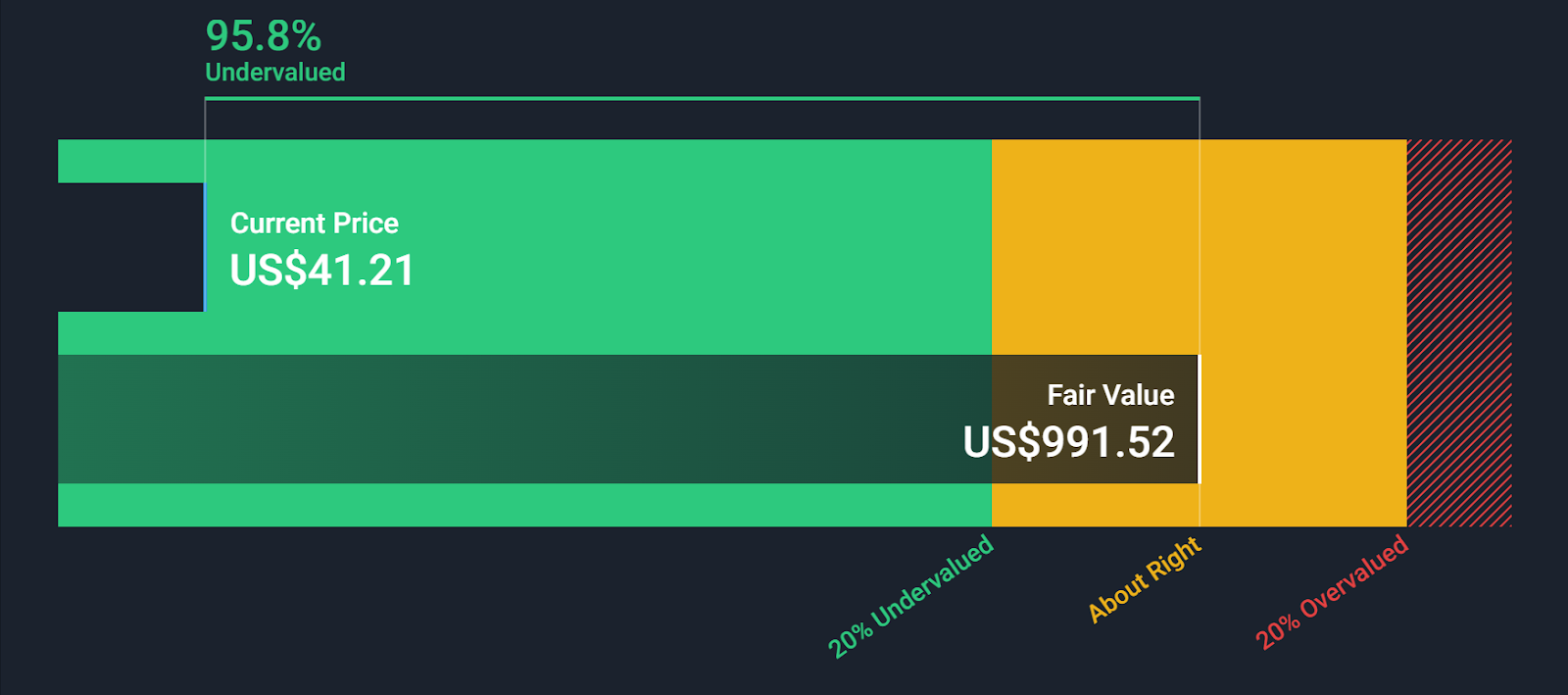

Simply Wall Street’s analysis echoes this sentiment, estimating that Euroseas trades at an almost unbelievable 95.8% discount to its fair value.

In general, it’s rare to find a business that combines operational excellence with such compelling valuation metrics. And while no investment is guaranteed, the fundamentals point to Euroseas as a company with as strong an upside potential as any in the market. In short, Euroseas is not just a solid shipping company—it’s a diamond in the rough.

Final Thoughts

The stock market today is flooded with fast-moving companies in flashy, disruptive industries, but this often diverts attention from simpler, grounded businesses that quietly deliver outstanding returns.

Consider Euroseas. Over the past year alone, the company has returned an impressive 66% to shareholders, with a five-year return of 872%. That’s more than Meta, Microsoft, or even Apple—giants that dominate the headlines.

No, Euroseas may not have the allure of a tech stock. In fact, a glance at their website might make you think they’re still in the early 2000s. But under the hood, this is a lean, remarkably well-run shipping company with an efficient business model and a disciplined acquisition strategy.

Led by President and CEO Aristides J. Pittas, Euroseas is not only preserving a rich family legacy that spans over 140 years but enhancing it, building a company that’s more resilient than ever. With an expanding global economy and the unending demand for reliable shipping, Euroseas is positioned for sustained leadership in this essential industry. While the latest fads might come and go, Euroseas’ enduring fundamentals suggest that it’s here to stay—possibly for another century and beyond.

Disclosure/Disclaimer

We are not brokers, investment, or financial advisers, and you should not rely on the information herein as investment advice. If you are seeking personalized investment advice, please contact a qualified and registered broker, investment adviser, or financial adviser. You should not make any investment decisions based on our communications. Our stock profiles are intended to highlight certain companies for YOUR further investigation; they are NOT recommendations. The securities issued by the companies we profile should be considered high risk and, if you do invest, you may lose your entire investment. Please do your research before investing, including reading the companies’ public filings, press releases, and risk disclosures. Information contained in this profile was provided by the company, and extracted from public filings, company websites, and other publicly available sources. We believe the sources and information are accurate and reliable but we cannot guarantee it. The commentary and opinions in this article are our own, so please do your research.

Copyright © 2024 Micro Math Capital, All rights reserved.